ARCHIVED – Chapter 4. Technology Case Results

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Content

EF2018’s Technology Case explores how a global shift towards low carbon energy technologies could impact future Canadian energy supply and demand trends. Canada is a relatively energy intensive economyFootnote 18, and a major producer of many forms of energy. This potential shift is an important uncertainty for Canadian energy projections.

The Technology Case assumes that countries across the world increasingly adopt new technologies and increase their actions to combat climate change, as outlined in the IEA’s World Energy Outlook 2017 “Sustainable Development Scenario”. This global shift has implications for energy markets such as crude oil and natural gas. Canadian energy supply and demand trends are influenced by this global context, as well as specific assumptions on cost reductions and adoption for new technologies in Canada. The Technology Case is designed to explore a key uncertainty for the future of Canada’s energy system, a faster transition to a lower carbon economy driven by increasing global climate action and faster technological progress than assumed in the Reference Case. It is important to note that it is unclear which technologies will gain wider adoption in the future, and this case is just one example among many possible pathways. This Case analysis is not a prediction or recommendation of certain policies, technologies, or outcomes.

Recent Context

Various technology, policy, and social trends over the past decade point to the potential for a global shift towards a lower carbon economy. This section outlines several examples of these trends.

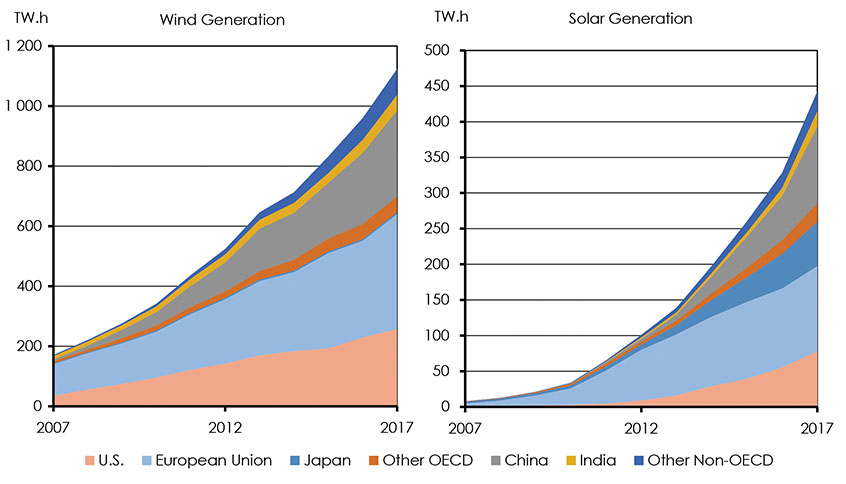

Falling costs and increased deployment of renewable electricity sources, like wind and solar, have been an important technology change. Figure 4.1 shows global wind and solar generation. Over the last decade, wind and solar power have increased substantially, initially led by the European Union and the U.S., with recent growth in China and Japan. Many global forecasting agencies see this trend continuingFootnote 19.

Figure 4.1: Global Solar and Wind Generation by Country, 2007-2017

Description

This graph shows global solar and wind generation by country from 1997 to 2017. In 1997 total global wind and solar generation was 12 and 0.8 TW.h respectively. In 2017 total global wind and solar generation was 1122.7 and 442.6 TW.h respectively.

Technology and policy changes are transforming the transportation sector. Many forecasting agencies expect growth in refined oil products demand (gasoline) to slow or decline compared to historical trends. These changes are a key reason the concept of "peak demand"–the year at which global demand for oil will reach its maximum–is currently a key discussion point in oil markets. Reasons for this trend include increasing fuel economy, increased biofuel blending, and possible increase of EV adoption.

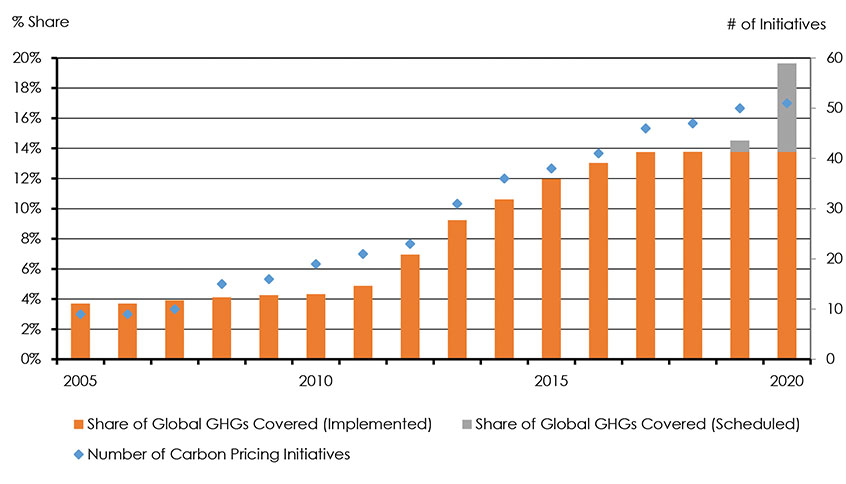

Emerging climate policies and future low carbon energy technologies are highly integrated. As an example of increasing momentum for policy action to reduce carbon emissions, Figure 4.2 shows that over the last decade the number of carbon pricing systems in the world increased from 10 to 46, while the coverage of those systems increased from 4% of global CO2 emissions to 14%. Carbon pricing systems scheduled to come into effect soon, led by China’s planned emission trading system, will bring this to over 50 systems covering nearly 20% of emissions by 2020Footnote 20.

Figure 4.2: Global Carbon Pricing Initiatives

Description

This graph shows the total number of carbon pricing initiatives from 2005 to 2020. In 2005 there were 9 carbon pricing initiatives globally, by 2020 it is estimated there will be 51 initiatives.

In the Canadian context, Natural Resources Canada's "Generation Energy" initiative highlights the integration of technology and policy factors, as well as the many broad social issues involved in transforming energy systems. The Generation Energy Council Report distills possible initiatives into four key pathways: wasting less energy, switching to cleaner power, using more renewable fuels, and producing cleaner oil and gas. The milestones outlined in these pathways will have significant implications for how energy is produced and consumed in Canada.

These trends suggest momentum towards a low carbon energy system. The Technology Case explores what continued momentum on this front might mean for future energy supply and demand in Canada.

Assumptions

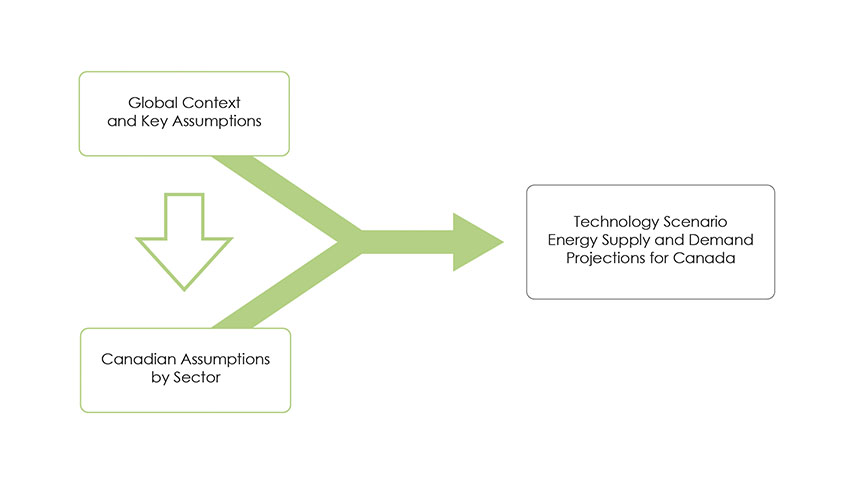

The Technology Case is based on a set of global and Canadian assumptions around energy markets, energy and climate policy, and adoption of low carbon technologies. Figure 4.3 illustrates the overall approach to the Technology Case.

- Global Assumptions: Includes energy market price assumptions for global crude oil and North American natural gas, economy-wide carbon pricing, and other general policy trends. These global assumptions are aligned with the IEA’s World Energy Outlook 2017 “Sustainable Development Scenario”. This scenario, consistent with the Paris climate a greement targets, shows a steep decline in emissions from 2020 to 2040, putting the world on track to hold the increase of global average temperatures to below 2 degrees. It does so while also balancing other sustainable development goals, in particular, increasing access to modern energy sources and reducing local air pollution.

- Canadian Assumptions: Includes new technology cost reductions and adoption, energy efficiency improvements, use of alternative fuels, and Canadian benchmark oil and gas prices. These Canadian-specific assumptions are chosen to be consistent with the global context, but also reflect the specific nature of the Canadian energy system.

Figure 4.3: Technology Case Overview

Description

This figure outlines the Technology Case assumptions. Both Global and Canadian assumptions by sector are included in formulating the Technology Case.

The Technology Case Assumptions are also summarized in Appendix B.

The Technology Case and Paris Climate Agreement Goals

EF2018’s global assumptions are aligned with the IEA’s Sustainable Development Scenario, which reflect a world on track to meet commitments made under the Paris climate agreement. The assumptions and outcomes of the Technology Case are broadly consistent with the type of outcomes expected in such a transition: declining fossil fuels use, increasing use of non-emitting fuels, increased energy efficiency, and emergence of new technologies.

However, EF2018 and the Technology Case are strictly focused on Canada. Since climate change is a global issue, it is difficult to assess global climate implications without undertaking an integrated global climate modeling exercise.

The Technology Case illustrates what a broad shift towards a low carbon energy system might look like for Canada. It is not a recommended pathway towards achieving Paris climate a greement goals, or Canada’s own GHG emission targets. ECCC produces the official analysis of Canada’s current emission outlook and performance against its climate commitments. Its most recent analysis can be found in Canada’s 7th National Communication and 3rd Biennial Report.

Global Assumptions

Global Policy and Technology Trends

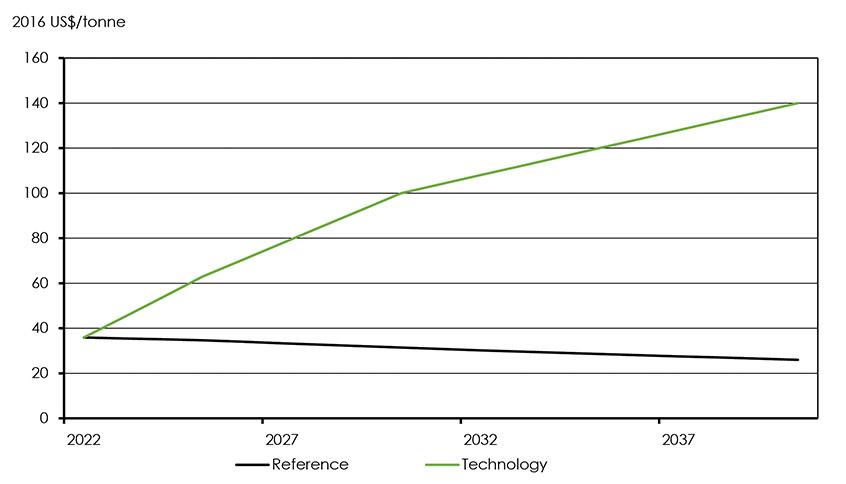

- Carbon Pricing: The IEA Sustainable Development Scenario shows a shift to a low carbon future that is driven by a broad set of policy assumptions, as well as the integration of a higher share of low carbon energy sources and technologies into the global energy mix. Carbon pricing provides a key driver for change across the economy. A rising carbon price is assumed for both OECD and non-OECD economies. Figure 4.4 shows the Technology Case assumption for Canada, aligned to the IEA’s OECD carbon price increase.

- Other actions: In addition to carbon pricing, the IEA outlines several high-level policy initiatives by sector, including efficiency regulations, support for alternative fuels, emission standards and limits, and reduction of fossil fuel subsidiesFootnote 21

Figure 4.4: Economy-Wide Carbon Price, Reference and Technology Cases, 2022-2040

Description

This figure shows the economy wide carbon price in Canada from 2022 to 2040 under the Reference and Technology Cases. In the Reference Case the carbon price is 36 US$/tonne in 2022 and decreases to 26 US$/tonne by 2040. In the Technology Case the carbon price is 36 US$/tonne in 2022 and increases to 140 US$/tonne in 2040.

Global Crude Oil and Natural Gas Markets

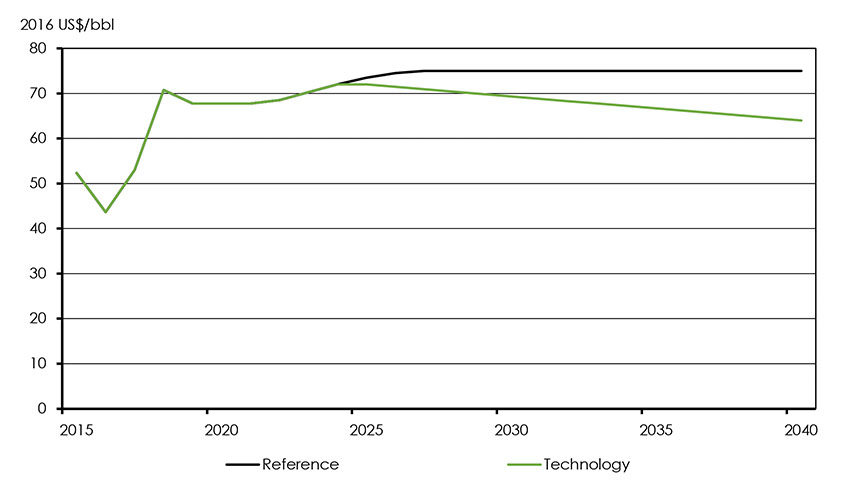

- Crude Oil Price: The Technology Case Brent price assumption aligns to the IEA Sustainable Development Scenario global crude oil price. It begins to trend downward after 2025, consistent with a declining demand for global crude oil. It falls to US$69/bbl in 2030, $6 lower than the Reference Case, and US$64/bbl by 2040, $11/bbl lower than the Reference Case (Figure 4.5).

Figure 4.5: Brent Price Assumptions, Reference and Technology Cases

Description

This figure shows the Brent oil price assumptions from 2015 to 2040 in the Reference and Technology Cases. In the Reference Case the price of Brent increases from $52.32 in 2015 to $75 in 2040. In the Technology Case the price increases to $64.

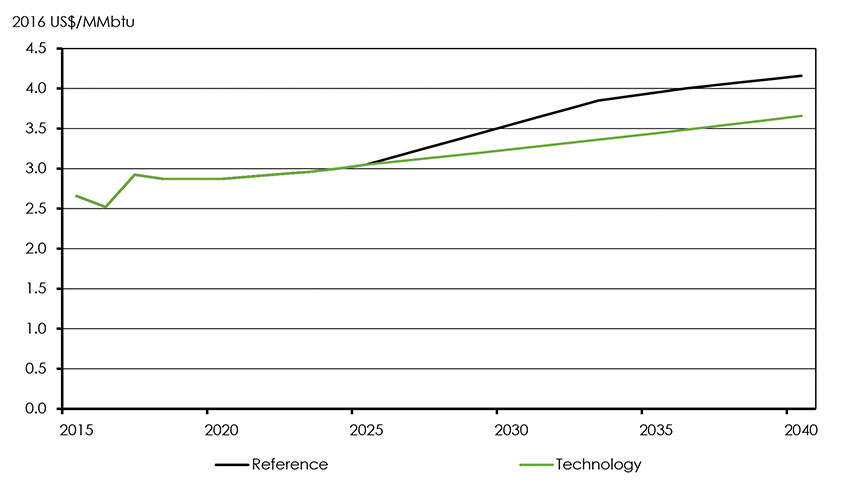

- Natural Gas Price: The natural gas price in the Technology Case aligns to the IEA Sustainable Development Scenario U.S. natural gas price. It increases from $3.25/MMbtu in 2030 to $3.66/MMbtu in 2040. This reflects growing demand for natural gas to replace coal for power generation. However, the IEA projects that global natural gas demand will grow at a slower rate in this case compared to other scenarios. The Technology Case reflects this dynamic; in 2030 it is $0.30/MMBtu lower than the Reference Case and in 2040 is $0.50/MMbtu lower than the Reference Case (Figure 4.6).

Figure 4.6: Henry Hub Price Assumptions, Reference and Technology Cases

Description

This graph shows the Henry Hub price assumptions from 2015 to 2040 in the Reference and Technology Cases. In the Reference Case the Henry Hub price increases from 2.66 US$/MMBtu in 2015 to 4.16 US$/MMBtu in 2040. In the Technology Case the price increases to 3.66 US$/MMBtu in 2040.

Canadian Assumptions

Canadian Energy Markets

- End-use Fuel Prices: Canadian end-use prices are affected by the carbon price and benchmark crude oil and natural gas price trends. Lower crude oil and natural gas prices put downward pressure on prices for refined products and delivered natural gas. Increased carbon pricing puts upward pressure on prices, based on the relative carbon intensity of fuels. Table 4.1 provides example carbon prices of various fuels in energy equivalent and volumetric terms.

| $30/tonne | $50/tonne | $90/tonne | $140/tonne | |||||

| Energy | Volume | Energy | Volume | Energy | Volume | Energy | Volume | |

| Natural Gas | 1.50 $/GJ | $1.58/Mcf | 2.49 $/GJ | $2.63/Mcf | 4.49 $/GJ | $4.74/Mcf | 6.98 $/GJ | $7.38/Mcf |

| Gasoline | 2.06 $/GJ | 7.1¢/L | 3.43 $/GJ | 11.9¢/L | 6.17 $/GJ | 21.4¢/L | 9.59 $/GJ | 33.2¢/L |

| Diesel | 2.22 $/GJ | 8.6¢/L | 3.70 $/GJ | 14.3¢/L | 6.67 $/GJ | 25.8¢/L | 10.37 $/GJ | 40.1¢/L |

- Canadian Benchmark Prices: The Technology Case assumes that the differentials between benchmark prices shown in Chapter 2 for the Reference Case are the same in the Technology Case. This implies a Technology WCS and CLS price $11/bbl lower than the Reference Case in 2040, and a NIT price $0.50/MMBtu lower in 2040. Given the global context, this is a very uncertain assumption. As the globe shifts towards a low carbon economy, market dynamics may evolve differently and lead to different relationships between the various benchmark prices in the short or long term.

- LNG Export Assumptions: The Technology Case assumes LNG export volumes are the same as the Reference Case. This is an area of uncertainty as well. Many dynamics will influence potential Canadian LNG exports, including economics, individual company investment decisions, and the role of natural gas globally in switching away from more carbon-intensive fuels like coal. LNG export assumptions are a key uncertainty in all EF2018 cases, and could be higher or lower than assumed both compared to the assumptions, and relative to each other.

Electricity Generation

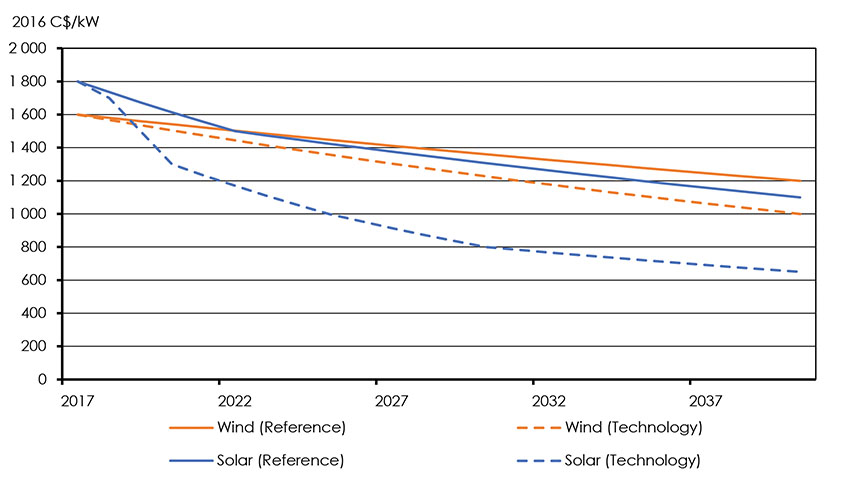

- Solar and Wind Capital Cost Reductions: Figure 4.7 compares wind and utility solar capital cost assumptions in the Reference and Technology Cases. In the Technology Case, wind costs decline nearly 40% compared to 2017 levels, while solar costs decline over 60%.

Figure 4.7: Wind and Solar Costs, Reference and Technology Cases, 2017-2040

Description

This graph shows wind and solar capacity costs from 2016 to 2040 in the Reference and Technology Cases. In 2016 solar and wind capacity costs were 1900 and 1700 C$/kW respectively. In the Reference Case solar and wind capacity costs fall to 1100 and 1200 C$/kW respectively. In the Technology Case solar and wind capacity costs fall to 650 and 1000 C$/kW respectively.

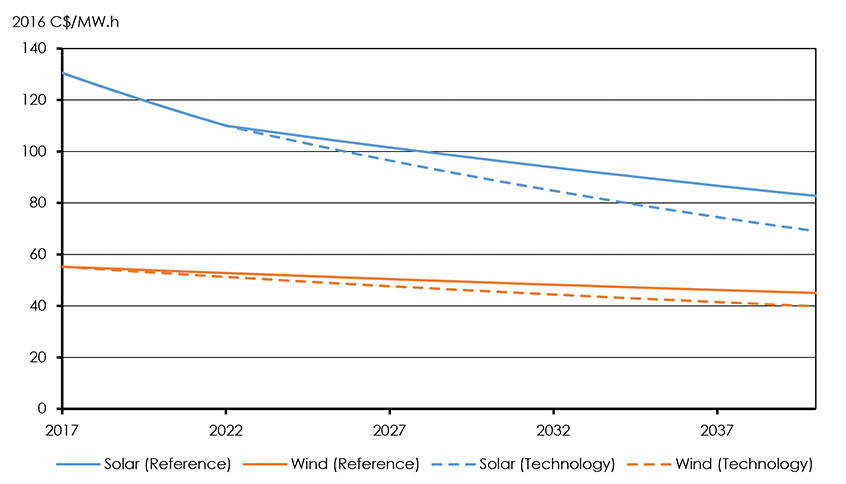

- Solar and Wind Levelized Cost Reductions: Figure 4.8 compares levelized costs of wind and solar power, which is the cost per MW.h of generation. It shows that falling capital costs drive generation costs for these resources. Levelized costs include the amount of generation each kW of capacity produces, or the capacity factor. In Canada, wind power generally operates at a higher capacity factor than solar. This implies that wind, on average, has a lower cost per MW.h generated than solar, even with a higher capital cost.Footnote 22

Figure 4.8: Wind vs Solar Levelized Cost, Reference and Technology Cases, 2017-2040

Description

This figure shows the levelized cost assumptions of wind and solar in the Reference Case compared to the Technology Case. Costs fall in both cases, although the decline is faster for the Technology case for both wind and solar. Solar costs begin at around 131 2016 C$/MWh and fall to 82 by 2040 in the Reference Case and 69 in the Technology Case. Wind costs fall from 55 2016 C$/MWh to 45 in the Reference Case and down to 40 in the Technology Case.

- Integrating Variable Renewables: The Technology Case assumes enhanced integration of wind and solar power into electricity grids. This includes additional electricity transmission between Canadian provinces, and a greater use of demand management to match electricity demand loads to variable renewable generation.

Variable Renewable Energy

Variable sources like wind and solar require additional efforts to integrate into the grid.

- Flexible generation: Generation sources like hydro and natural gas can be ramped up when solar and wind generation declines, or down when it increases.

- Transmission: Variable generation is location specific. Increased transmission from areas where wind generation is higher can help smooth out the variability of the resource, or connect the region to additional flexible generation. Recent analysis found transmission to be a key element of decarbonizing electricity grids for both CanadaNote a and the U.S.Note b

- Demand side management: Electric loads can possibly be adjusted to better align with generation. As end uses become increasingly digitized, renewables could be better integrated for both large scale loads, and smaller scale integration at the household level.Note c

- Storage: Grid-scale storage includes many technologies like pumped hydro, batteries, compressed air and flywheels. Storage can help balance the electricity system by charging and discharging as wind and solar levels fluctuate. Recently, there is increasing interest in battery storage, given decreasing costs. The learning rate of battery storage–the percentage costs have fallen for every doubling of global battery storage capacity–has been at similar levels to solar PV.Note d

Oil and Gas Production

- Global competition: The global context of the Technology Case includes higher carbon prices and lower crude oil and natural gas prices compared to the Reference Case. This implies increased competitive pressures for producing these resources at a lower cost, as well as at reduced emission levels. Since this Case assumes the world is moving towards widespread action on climate change, current Canadian measures to avoid adverse competitiveness issues, or carbon leakage, are phased out by 2035. This includes the output based allocations (OBAs) used in the Alberta Carbon Competitiveness Incentive Regulation, as well as the federal backstop.

- Solvent Technology for In Situ Production: The Technology Case assumes widespread adoption of solvent technology for oil sands in situ production. Steam solvent technology is applied to all new production by 2025, as well as some existing reservoirs, resulting in a 25% reduction in SOR. By 2030, pure solvent technology reaches wide-scale commercial adoption, and all new production employs this technology, leading to an 80% reduction in SOR.

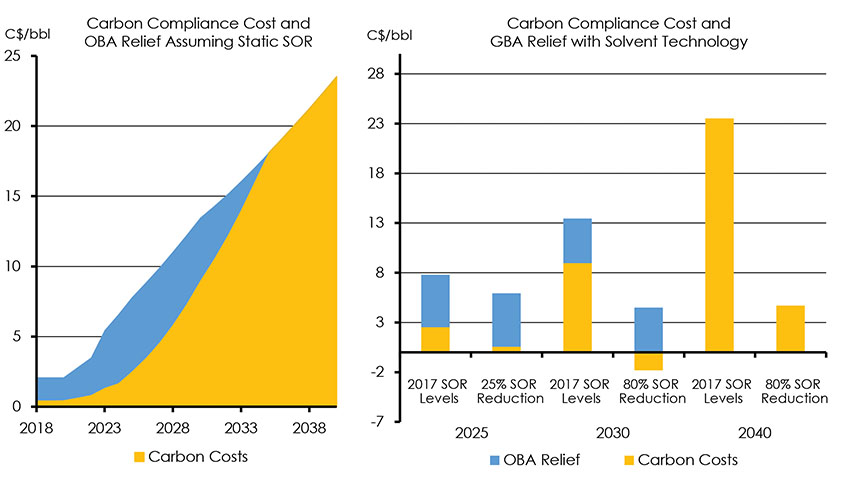

Figure 4.9 illustrates this incentive to reduce the carbon emissions in the Technology Case. The first chart shows the theoretical carbon cost per barrel in the Technology Case assuming OBAs are phased out, carbon price rises, and emission intensity of production remains at 2016 levels. Given the oil prices shown earlier, these costs would become a major impediment to production economics. The second chart shows that 25% and 80% SOR reductions from steam and pure solvent technology, respectively, can reduce those costs significantly.

Solvent Technology

These technologies involve displacing the steam that is injected to produce oil with solvents, lowering natural gas requirements to generate the steam, and therefore the emissions intensity of production. Both steam and pure solvents are emerging technologies that have been under development for a number of years. An in situ project using steam-solvent technology can have higher upfront costs than a traditional in situ project as a result of additional facilities to store, treat, and recover solventsNote a. Greater bitumen recovery rates and lower steam requirements can offset those costs to varying extents depending on individual project characteristics. Pure solvents also offer the potential for capital cost reductionsNote b.

Figure 4.9: Emission Cost Per Barrel Under Business As Usual, 25% Reduction, and 80% Reduction In Emission Intensities, Given Technology Case Carbon Costs

Description

These two graphs show the incentives that companies face to reduce carbon emissions in the Technology Case while assuming output-based allocations are phased out completely by 2035. The first illustrates the theoretical carbon costs per barrel of oil, which assumes no reduction in the SOR, increases from 2 C$/bbl in 2018 to 23.5 in 2040. The relief provided by Output Based Allocations (OBA’s) begins as 1.7 C$/bbl in 2018 and is phased out in 2035.

The second shows that steam oil ratio reductions from improved technology can greatly reduce these costs. If these ratios are reduced by 80% then compliance costs will by 4.7 C$/bbl compared to 23.5 with no reductions by 2040. If these ratios are reduced by 25% then compliance costs will be 0.6 C$/bbl with 5.4 C$/bbl covered by OBA relief by 2040.

Residential and Commercial Energy Efficiency

- Energy Efficiency Improvements: The Technology Case assumes significant efficiency improvements across the buildings sector. Reducing energy and emissions intensity for buildings is an important part of many climate action plans, including the Pan-Canadian framework. The Technology Case assumes improvements to windows, building shells, and insulation reduce the energy required for heating and cooling. For remaining energy requirements, energy using devices (space and water heating, cooling, and appliances) become more efficient.

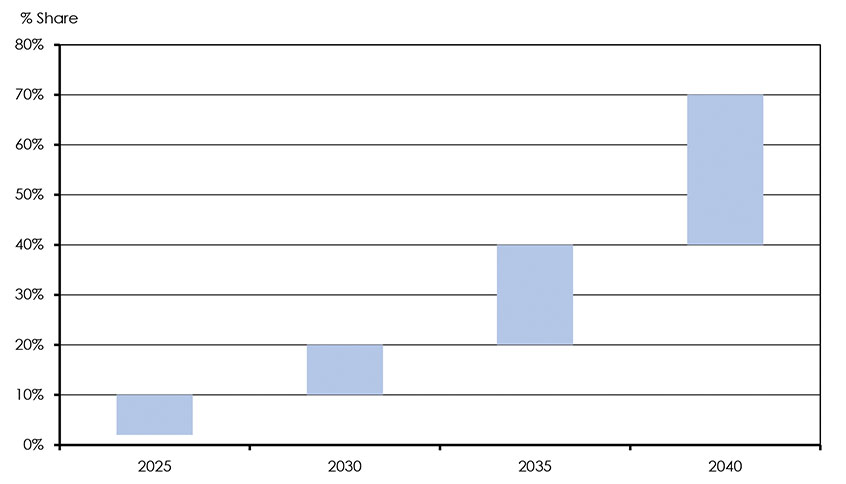

- Increased Heat Pump Adoption: Figure 4.10 illustrates the range of heat pump adoption across provinces in the Technology Case. Adoption of heat pumps increases from 10 to 20% of new, and replacement systems, by 2030; then it rapidly increases from 40 to 70% by 2040. The Technology Case assumes that technology improves for cold climate heat pumps, as well as reduced upfront costs. Analysis for the U.S. suggests heat pump costs could fall 10 to 20% by 2025-2030, and 20 to 30% by 2040. For areas that rely heavily on natural gas for heating, hybrid natural gas heat pump systems are an option. These systems rely on electric heat pumps producing heat when electricity prices are low, and high-efficiency natural gas during peak times when electricity prices are high.

Heat Pump Technology

Increased adoption of heat pumps for space heating and cooling, and heating water, could be an important component of decarbonizing Canada’s building sector. Heat pumps have an advantage in that rather than creating heat, they exchange energy by extracting heat from an outside source and pumping it into a space. Heat pumps use approximately half the electricity compared to baseboard heating to generate the same amount of heat. They are not currently found more broadly because they are relatively more expensive compared to baseboard heating or natural gas furnaces, and have reduced efficiency during cold weather. Relatively low prices of natural gas compared to electricity can prevent electric heat pumps from yielding cost savings compared to high efficiency natural gas furnaces.

Figure 4.10: Range of Heat Pump Adoption Across Provinces, Technology Case

Description

This figure shows the adoption rate of heat pump technology adoption across all provinces from 2025 to 2040. From the present until 2025 the rate increases from 2% to 10%. This increases to 20% in 2030, 40% in 2035, and 70% in 2040.

- Process improvements and digitization: Increased levels of digitization allow for less energy waste, optimizing energy use and energy costs (for example, load shifting when excess solar and/or wind power is available), and integration with other forms of energy demand, such as EV charging.

Transportation

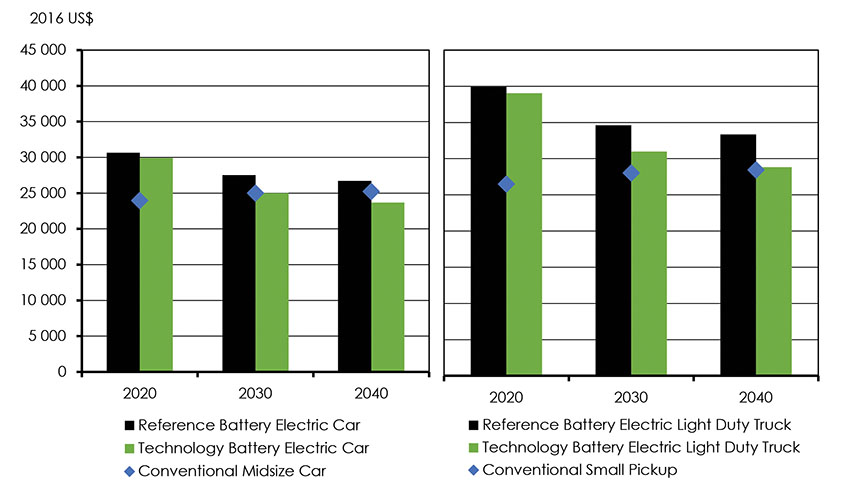

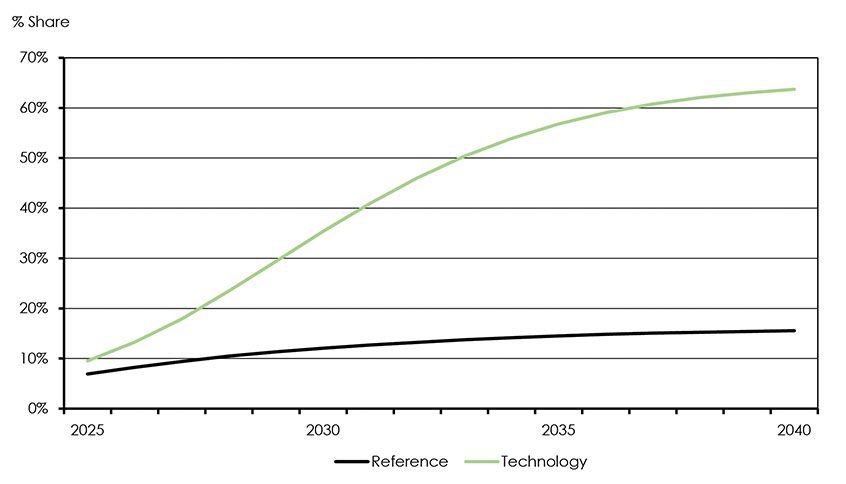

- Electric Vehicles: Figure 4.11 shows the assumed average cost for an EV in the Reference Case compared to a representative internal combustion engine (ICE) car and truck. On an average cost basis, EV purchase price reaches ICE levels by 2030 for cars and 2040 for trucks. Given the impact of end-use prices, and that the per-unit driving cost and maintenance cost of EVs are assumed to be lower than ICE, the economics begin to favour electricity in this time frame. In the 2030s, the Technology Case assumes charging infrastructure is well developed, leading to a rapid increase in the share of EVs in that decade. Increased ride sharing, mobility as a service, and potential autonomous vehicle technology could also favour electric vehicle adoption. Figure 4.12 shows average new sales of EVs in the Reference Case compared to the Technology Case.

Figure 4.11: Average Vehicle Purchase Price, Battery Electric Cars and Light Duty Trucks, Reference and Technology Cases

Description

In these two graphs the cost of battery electric vehicles (BEV) in the Reference and Technology Cases is compared to the price of an internal combustion vehicle (ICE). The left graph shows that the cost of a BEV car in the Technology Case is projected to fall from 30,000 2016 $US in 2020 to 25,000 in 2030 and 24,000 in 2040. It falls to 28,000 in 2030 then 27,000 in 2040 in the Reference Case. The price of a conventional ICE car increases from 24,000 2016 $US to 25,000 over the same period.

In the graph on the right the cost of a BEV truck is compared in the same manner. BEV truck costs fall from 40,000 2016 US$ to 35,000 then 33,000 in the Reference Case and from 39,000 to 35,000 then 29,000 in the Technology Case. The cost of a conventional truck rises from 26,500 to 28,500 over the same period.

Figure 4.12: Share of EVs in New Passenger Vehicles, Reference vs Technology Case, 2025-2040

Description

Starting in 2025 this chart shows the share of new car sales that electric vehicles make up in the Reference and Technology Cases. In the Technology Case the share reaches 64% by 2040 from 10%, and in the Reference Case the share of sales rises to 15% from 7%.

- Fuel Economy Improvements: The Technology Case assumes ICE vehicles continue to improve and reduce their own variable costs, building upon the efficiency improvements from current vehicle emission standards. The Technology Case assumes fuel economy of gasoline and diesel cars and trucks improves by 1.5% per year in the longer term, beyond the expiration of current emission standards for light duty vehicles (2025) and heavy-duty trucks (2028).

- Alternative Fuels: Biofuel blending continues to grow, with ethanol and biodiesel blending reaching 10% by 2025. By 2040, gasoline and diesel are blended with 15% renewable fuels on averageFootnote 23.

- Aviation: Biofuels are currently being used for some air travelFootnote 24, and this increases in the Technology Case. Improved efficiency, as well as biofuel blending to 15% of jet fuel by 2040, reduce the emissions intensity of air travel.

Northern Territories and Remote Communities in the Technology Case

Northern Territories and remote communities have unique energy contexts with higher costs due to fuel transportation costs, colder climates, and reduced energy options, particularly for communities not connected to utility grids. Reducing reliance on diesel is a key complementary action in the Pan-Canadian Framework. The 2018 Energy and Mines Ministers Conference featured items on adopting renewables and reliability, as well as integrating new technology in remote communities.

Given these unique energy issues, the Technology Case includes some specific assumptions for Northern Territories. The Technology Case assumes an increase in solar and wind power over the longer term, offsetting large amounts of diesel generation in the summer months. For space heating, current trends towards increasing biomass use are strengthened. On the energy use side, the Case assumes a lower adoption of EVs and heat pumps compared to the other provinces, but similar improvements in energy efficiency.

Industrial (Excluding Oil and Gas Production)

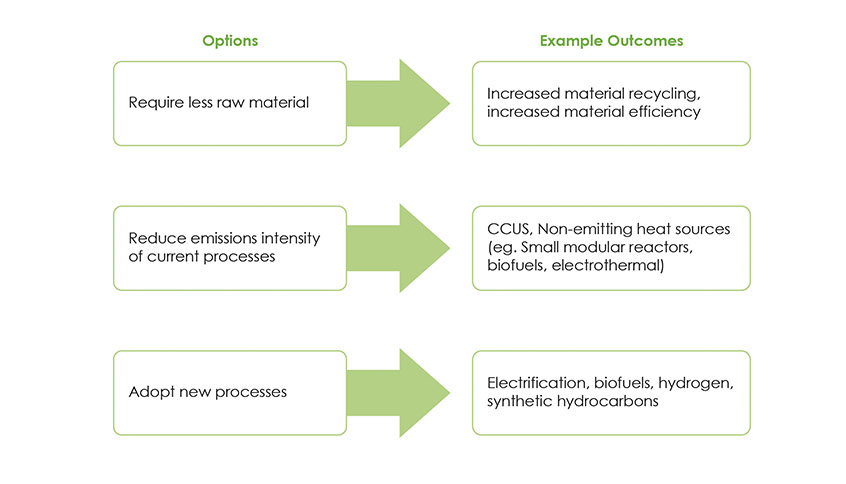

- Options for Emission Reductions: Canada’s industrial sector is composed of many different industries that all have unique energy issues, varying energy mixes, and different technological options for reducing or eliminating GHG emissions. Figure 4.13 provides a high-level view of options for industrial decarbonization summarized by a recent studyFootnote 25. The future energy mix for industry will depend on factors such as ability to recycle raw materials, change process or fuels, or adopt new technologies such as CCS and carbon capture, use and storage (CCUS). The various economics involved in these decisions depend on the circumstances of the individual operation, company, and industry. For example, industries in western Canada have easier access to suitable locations for CCS based on storage availability, while abundant hydropower in Quebec could make it an attractive location to explore electrification of processes.

Figure 4.13: Energy-intensive Industry Decarbonisation Options

Source: Bataille, et al

Description

This image shows decarbonisation options for energy intensive industries. This includes using less raw materials and increasing recycling along with efficiency. Reducing emissions intensity of current processes by using CCUS and non-emitting heat sources. And adopting new processes such as electrification, biofuels, hydrogen power, and synthetic hydrocarbons.

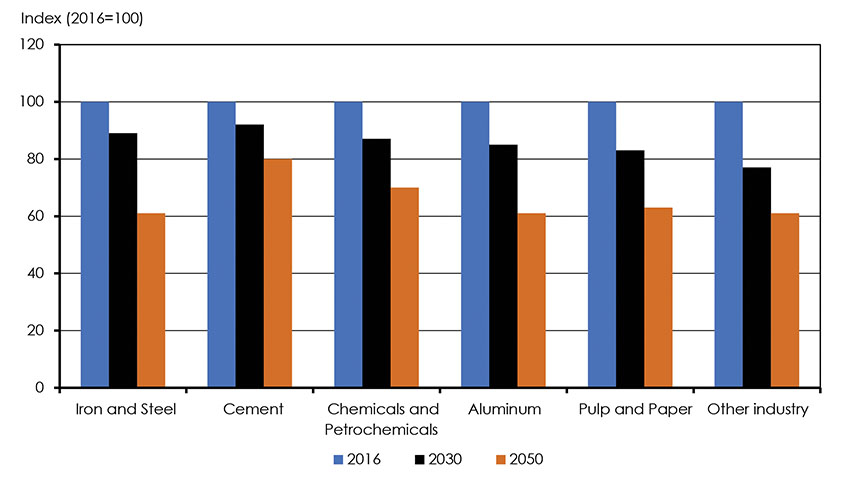

- Improved Energy Efficiency: Energy efficiency and adopting best available technologies will also play a key role. Figure 4.14 shows recent IEA analysis for Canada, comparing energy intensity in 2016, 2030 and 2050. The IEA suggests in a high efficiency scenario, energy intensity of various industries could fall relative to 2016 levels, showing some variation depending on the industry. The Technology Case assumes that average process and device efficiency increases by 5 to 10% relative to the Reference Case in 2025, and 15 to 30% by 2040. Process changes, such as increased material recycling, are assumed to reduce energy demands.

Figure 4.14: Canadian Industry Energy Intensity Reductions Relative to 2016, IEA Energy Efficiency Scenario, 2030 and 2050

Source: IEA

Description

This figure shows the relative decrease in energy intensity that various Canadian industries are projected to experience in a recent International Energy Agency report from 2016 to 2050. The iron and steel sector decreases in intensity by 11% in 2030 and 28% in 2050. Cement decreases by 8% and then 12%. Chemicals and petrochemicals falls by 13% and 17%. Aluminum decreases 15% then an additional 15%. Pulp and paper sheds 17% then 20%. And finally other industries fall 23% then 16%.

Multi-sector Technologies

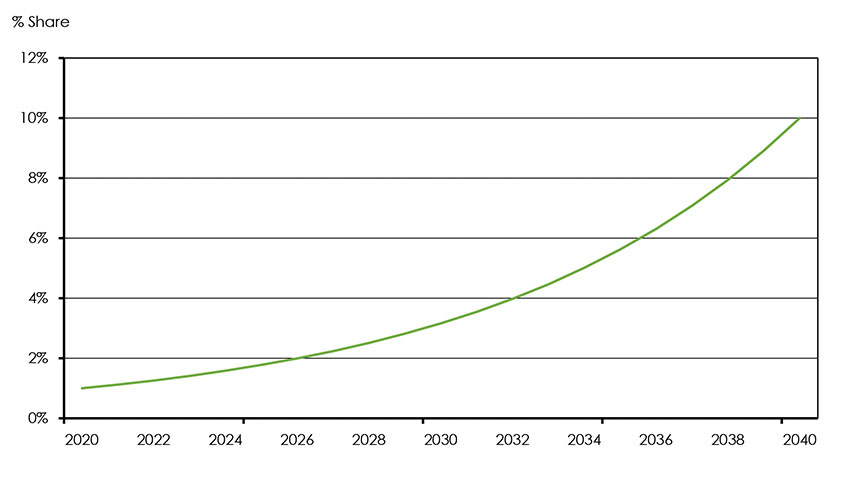

- Renewable Natural Gas (RNG) Blending: Costs of RNG vary by production type, and typically range between $8 and $20 per GJ. Although the lower end of that range is still higher than benchmark natural gas prices, as carbon costs rise and technology improves in the longer run, the relative economics of RNG could improve. The Technology Case assumes an average blending of RNG in Canada’s marketable gas mix of nearly 2% by 2025, 3% by 2030, and 10% by 2040. Figure 4.15 shows the rate of RNG blending in the Technology Case.

Figure 4.15: Renewable Natural Gas Blending Rate, Technology Case

Description

This chart shows the renewable gas blending rate in the Technology Case, which starts at 1% in 2020 and then rises to 10% in 2040.

Renewable Natural Gas

RNG is carbon neutral methane gas derived from captured organic waste. It can be produced from agriculture, forestry, and municipal waste sources. Impurities are then removed to meet necessary specifications for transportation, distribution, and use. Canada has several existing RNG facilities, and some distributors offer RNG blending as a consumer service.

Carbon Capture Technology: CCS and CCUS is another technology group that could gain significant momentum in a global shift towards a low carbon future. CCS and CCUS is often a critical component of energy scenarios that achieve low carbon futures. The Technology Case assumes technological progress and cost reductions for CCUS technology, with an additional 10 megatonne (MT) captured by 2030, and 45 MT by 2040.

Carbon Capture Use and Sequestration in Canada

Several commercial scale projects exist in Canada:

- Saskatchewan: The Boundary Dam power station began operations in 2014. The 115 MW coal-fired power plant is capable of capturing 1.3 MT of CO2 per year. Most of the CO2 from the facility is transported to nearby oil fields and used for enhanced oil recovery (EOR), while some is also stored underground in geological formations near the plant. In addition, Saskatchewan has also been importing CO2 by pipeline for EOR from a coal gasification plant in North Dakota.

- Alberta: The Quest Project captures CO2 from Shell’s Scotford upgrader and transports it by pipeline for permanent storage underground. The project is designed to capture up to 1.1 MT of CO2 per year or roughly 35% of the upgrader’s emissions. Under development is the Alberta Carbon Trunk Line, a 240 km pipeline that will transport CO2 from an industrial area north of Edmonton to EOR projects in central Alberta. Starting in 2018, the project will transport 1.7 MT CO2 per year captured from two facilities, the Sturgeon Refinery and an Agrium fertilizer plant. The pipeline has a capacity of nearly 15 MT per year to allow for future CCS projects.

The momentum for this technology has also been varied. As discussed in Chapter 2, Saskatchewan announced in 2018 that it would no longer be going ahead with planned CCS projects in the near future. Internationally, the IEA’s Tracking Clean Energy Progress lists CCUS in power and industry alike as “Not on Track.” Research and development on CCS and CCUS is ongoing. For example, May 2018 saw the opening of the Alberta Carbon Conversion Technology Centre, a research facility located near Alberta’s largest natural gas-fired power plant (Shepard Energy Centre), which will test capture and conversion technologies to turn emissions from the plant into useful products.

Results

The various energy market, policy, and technology assumptions that make up the Technology Case impact the energy supply and demand outlook in many ways. Figure 4.16 highlights four key shifts in the energy system:

- Total energy use declines: Compared to 2017 levels, total Canadian energy consumption is nearly 20% lower in 2040 despite similar total GDP and population trends.

- The share of renewable and non-emitting energy increases: Fossil fuel use falls faster than total energy demand, and by 2040 fossil fuel demand is 30% lower than 2017 levels. More efficient processes and technologies, as well as switching to renewable energy, cause this trend.

- By 2040, energy use per capita is reduced by one third, energy use per $ of GDP is nearly cut in half: Economic and population growth become further decoupled from energy use, as Canadian homes and businesses use energy more efficiently.

- Prices and technologies will shape Canada’s role in supplying oil and gas in a transitioning world: Canadian oil and gas production will be influenced by their ability to reduce costs and emissions. Technologies such as solvent-based injection for oil sands production provide an opportunity to maintain production, while market prices are a key uncertainty.

Figure 4.16: Technology Case Key Results

Description

The top left figure shows how total energy use changes in the Reference and Technology Cases from 2015 to 2040. Energy use increases from 13,300 PJ in 2015 to 14,200 in 2040. In the Technology Case total use decreases to 11,100 PJ with 4,100 made up of non-emitting fuels and renewables and the remaining 7,000 consisting of fossil fuels.

The chart on the top right shows the change in primary energy use by fuel. Fossil fuel use falls from 10,000 PJ in 2017 to 8,900 in 2030 and, 7,100 in 2040. Renewables and non-emitting resource use increases from 3,400 in 2017 to 3,800 in 2030 and, 4,100 in 2040. The graph on the bottom left shows the change in energy intensity in 2040 relative to 2017 in terms of energy use per $ GDP and energy use per person. Energy use per GDP falls 44% by 2040 and energy use per person falls by 31%.

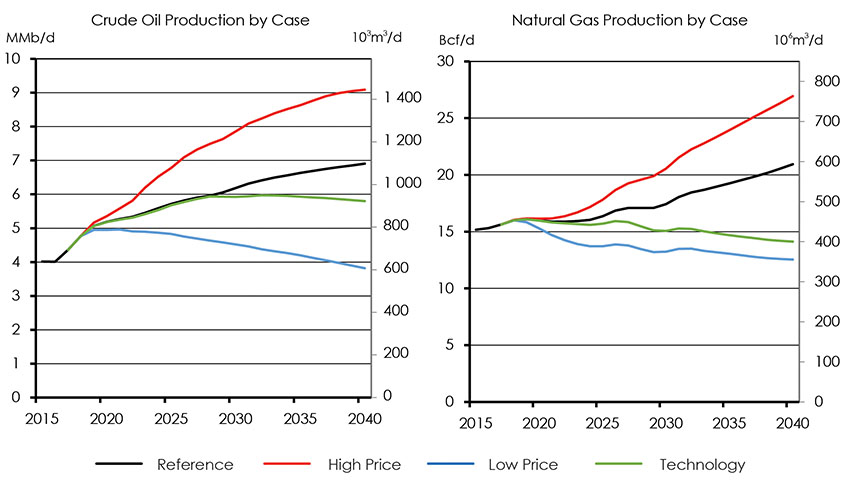

The chart on the bottom right shows crude oil production in the four cases from 2015 to 2040. In the Reference Case production climbs from 4 MMb/d to 6.9 in 2040. In the High Price Case it climbs to 9.1 MMb/d. In the Technology Case production peaks in 2029 at 5.9 MMb/d then falls to 5.8 in 2040. In the Low Price Case it peaks at 5.0 MMb/d in 2021 before falling to 3.8 in 2040.

Macroeconomic Drivers

Most macroeconomic drivers are similar between the Reference and Technology Case (Table 4.2). This is driven by improved technologies reducing energy use costs, but also several important assumptions. The Technology Case assumes global growth is the same as the Reference Case, including that of key trading partners. Revenues from the higher degree of carbon pricing in the case is recycled back into the economy through personal and corporate tax cuts. These factors result in small differences between macroeconomic trends between the Reference and Technology cases at the national level.

| Reference | Technology | |

| Real GDP | 1.8% | 1.8% |

| Population | 0.8% | 0.8% |

| Residential Floorspace | 1.4% | 1.4% |

| Commercial Floorspace | 1.9% | 2.0% |

| Exchange Rate (US$/C$, Average) | $0.82 | $0.80 |

End Use Energy Demand

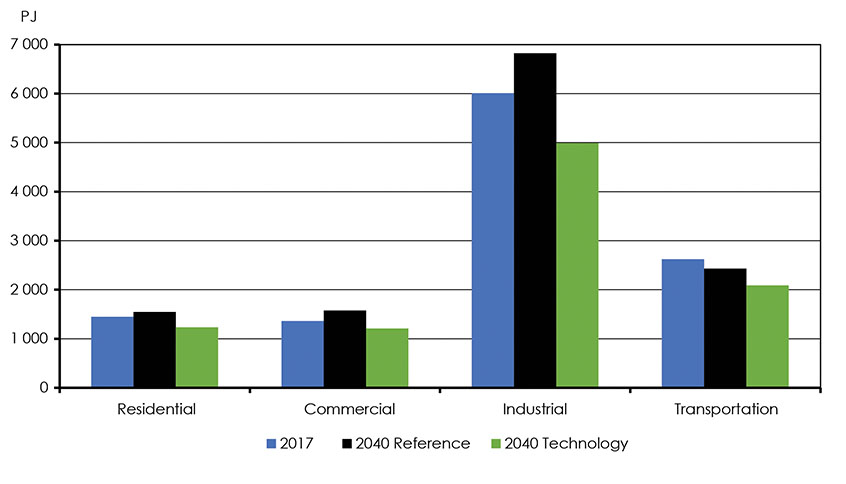

Figure 4.17 compares Technology Case demands in 2040 to 2017 levels, as well as the Reference Case projections for 2040. In the Technology Case, end-use energy demand declines relative to 2017 levels in all sectors. Demands are also below Reference Case levels.

Figure 4.17: Demands by Sector, Reference vs Technology Case

Description

This chart shows the change in end use energy demand from 2017 to 2040 in the residential, commercial, industrial, and transportation sectors in both the Reference and Technology Cases. In the residential sector 2017 demand is 1450 PJ and increases to 1550 in the Reference Case but falls to 1230 in the Technology Case. Commercial demand begins at 1360 PJ and rises to 1570 in the Reference Case while falling to 1210 in the Technology Case. The industrial sector sees a rise from 6010 PJ to 6820 in the Reference Case and a decrease to 4970 in the Technology Case. And in the transportation sector use falls from 2620 PJ to 2430 in the Reference Case and 2090 in the Technology Case.

Residential and Commercial

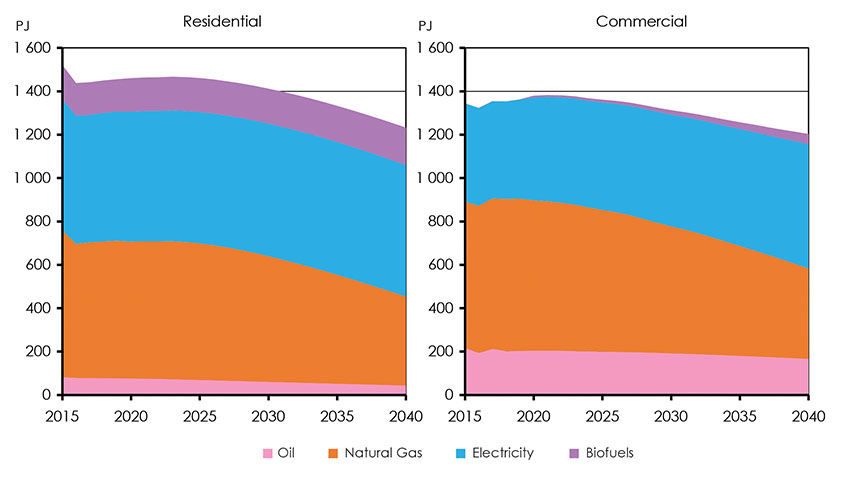

Improving efficiency and increased electrification via high efficiency heat pumps leads to residential and commercial demands being 15% and 11% lower in 2040 than their 2017 levels, respectively. Figure 4.18 shows residential and commercial demand by energy source in the Technology Case.

When heat pumps replace natural gas heating, they lead to higher electricity use, although at lower levels than the natural gas they are displacing. However, when heat pumps replace electric baseboard heating or conventional air conditioning, this reduces electricity demand. Appliance efficiency improvements put further downward pressure on electricity requirements. Overall, despite electrification, annual electricity demands are similar to Reference Case levels. Given that demands for other heating fuels fall faster than electricity in the Technology Case, electricity makes up a growing share of residential and commercial building demands .

Figure 4.18: Residential and Commercial Demands by Energy Source, Technology Case

Description

The chart on the left shows the change in residential energy demand by source from 2015 to 2040 in the Technology Case. Oil demand decreases from 82 PJ to 43. Natural gas demand falls from 677 PJ to 410. Electricity demand stays constant at 606 PJ. Biofuels demand increases from 157 PJ to 173. The second chart shows the energy demand in the commercial sector over the same period. Here oil demand falls from 216 PJ to 166. Natural gas demand falls 675 PJ to 417. Electricity demand rises from 453 PJ to 573 PJ. And Biofuels demand rises from 0 PJ to 46.

Transportation

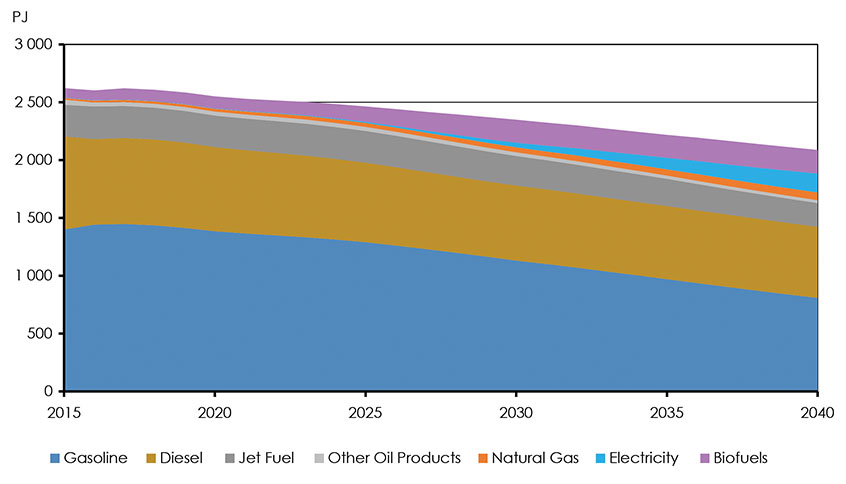

In the transportation sector, increased use of biofuels and electricity diversifies the fuel mix of the sector that has long been dominated by oil-based petroleum products. Energy efficiency improvements for all forms of travel also reduce energy requirements. Figure 4.19 illustrates the transportation sector energy mix in the Technology Case.

Figure 4.19: Transportation Demands by Fuel, Technology Case

Description

This graph shows transportation demand by fuel in the Technology Case from 2015 to 2040. Gasoline demand drops from 1400 PJ to 809. Diesel consumption falls from 804 PJ to 615. Jet fuel slightly declines from 274 PJ to 205. Demand for other oil products slows from 44 PJ to 25. Natural gas demand increases from 15 PJ to 66. Electricity demand sees a dramatic rise from 3 PJ to 164. And biofuels demand rises from 82 PJ to 204.

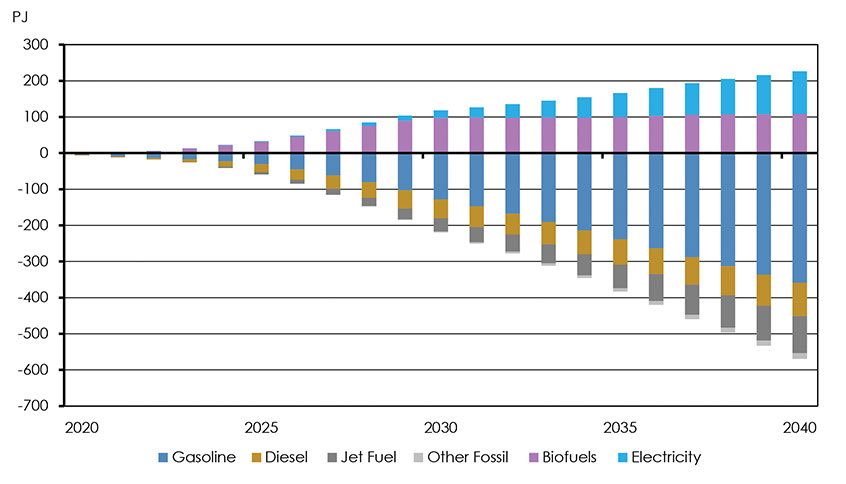

Increased EV penetration adds approximately 120 PJ, or over 30 TW.h, of annual electricity use by 2040. This reduces a relatively higher amount of gasoline and diesel, as EVs typically use less energy per km travelled compared to conventional vehicles. Improved vehicle efficiency and biofuel blending further reduces demand for these fuels. Relative to the Reference Case by 2040, Figure 4.20 shows that the Technology Case adds nearly 230 PJ of electricity and biofuels, which is more than offset by a 570 PJ decrease in petroleum product demand.

Figures 4.20: Difference in Transportation Demands by Fuels, Technology and Reference Cases

Description

This chart shows the difference in transportation fuel demand between the Technology and Reference Cases from 2020 to 2040. The difference in demand between the cases for all fuels is less than 5 PJ in 2020 but grows over the projection period. Gasoline demand is 359 PJ higher, diesel demand is 92 PJ higher, jet fuel is 103 PJ higher, and other fossil fuel demand is 16 PJ in the Reference Case. While biofuels and electricity demand are 108 and 118 PJ higher in the Technology Case.

Industrial

Figure 4.21 shows industrial demand in the Technology Case by fuel. This reflects changes in energy use in both the oil and gas production sector as well as other industrial sectors. By 2040, industrial energy use is nearly 15% lower than 2017 levels, and 20% lower than the Reference Case. This is due to lower oil and gas production that is produced using less energy, as well as improved processes in other energy intensive industrial sectors.

Figure 4.21: Industrial Demands by Fuel, Technology Case

Description

This graph shows annual industrial energy demand by fuel type from 2015 to 2040 in the Technology Case. Coal demand falls from 143 PJ to 100. Oil demand falls slightly from 1861 PJ to 1730. Natural gas use significantly falls from 2523 PJ to 1804. Electricity on the other hand sees demand increase from 845 PJ to 916. Biofuels increase 314 PJ to 440.

Crude Oil and Natural Gas Production

In the Technology Case, oil and natural gas producers face lower prices than in the Reference Case, reflecting slower growth in gas and declining demand for oil. Markets and infrastructure uncertainty are reflected in Canadian price discounts, which are the same as the Reference Case. In this smaller, and therefore increasingly competitive, global market for oil and gas, crude oil and natural gas production are lower than the Reference Case. By 2040, Technology Case crude oil production is 15% lower than Reference Case levels, and natural gas production is over 30% lower. However, production in the Technology Case is higher than the Low Price Case, highlighting the importance of market dynamics in future production trends.

Figure 4.22: Total Oil and Gas Production, All Cases

Description

The chart on the left shows crude oil production in the four cases from 2015 to 2040. In the Reference Case production climbs from 4 MMb/d to 6.9 in 2040. In the High Price Case it climbs to 9.1 MMb/d. In the Technology Case production peaks in 2029 at 5.9 MMb/d then falls to 5.8 in 2040. In the Low Price Case it peaks at 5.0 MMb/d in 2021 before falling to 3.8 in 2040.

The graph to the right shows Canadian natural gas production over the same time period. In the Reference Case production rises from 15 Bcf/d to 21 in 2040. The High Price Case sees more rapid growth and reaches 27 Bcf/d by the same date. In the Low Price Case gas production peaks in 2018 at 16 Bcf/d, then falls to 12.5. In the Technology Case production peaks in 2019 at 16 Bcf/d then declines to 14 by 2040.

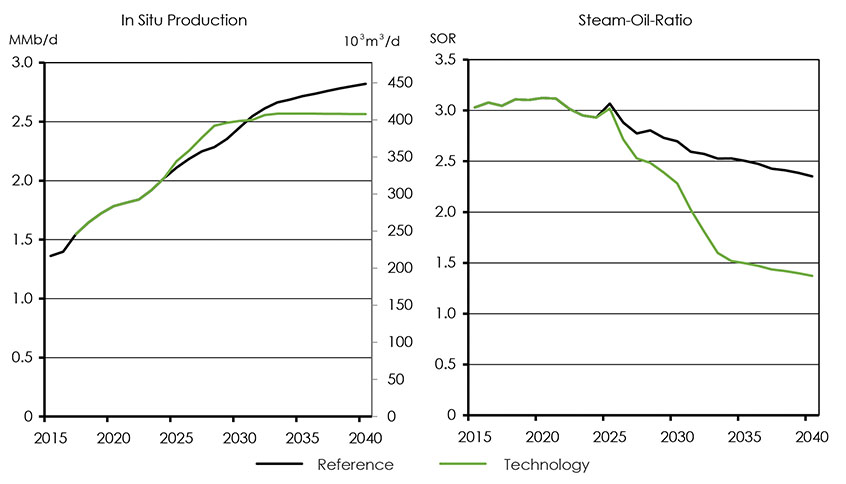

The key technology assumption of steam solvents being widely deployed by 2025 and pure solvents by 2030 has two main effects on oil sand producers. First, the technology creates a production uplift, so more oil is produced using the technology than standard steam injection, possibly up to 30%. Second, the technology reduces SORs. Figure 4.23 shows in situ production and SOR trends. In the medium term, technology improvements dominate market impacts, and Technology Case production is higher than the Reference Case until 2030. Over the longer term, lower prices and higher costs of carbon emissions cause Technology Case in situ production trends to flatten out. By 2040, in situ production in the Technology Case is nearly 10% lower than the Reference Case, but still higher than current levels.

Figure 4.23: In Situ Production and SOR Trends, Reference vs Technology

Description

The chart on the left illustrates oil sands in situ production from 2015 to 2040 in the Technology and Reference Cases. In the Technology Case production increases from about 1.4 MMb/d in 2015 to around 2.6 in 2028 where it remains relatively stable with only minor increases through 2040. In the Reference Case production climbs continuously and reaches 2.8 MMb/d in 2040.

The figure on the right shows the projected steam oil ratio (SOR) used for in situ production in the Technology and Reference Cases from 2015 until 2040. The SOR remains constant for both at close to 3 until 2024, when they diverge. After this point the Technology Case drops to 1.4 by 2040 and the Reference Case drops to 2.4.

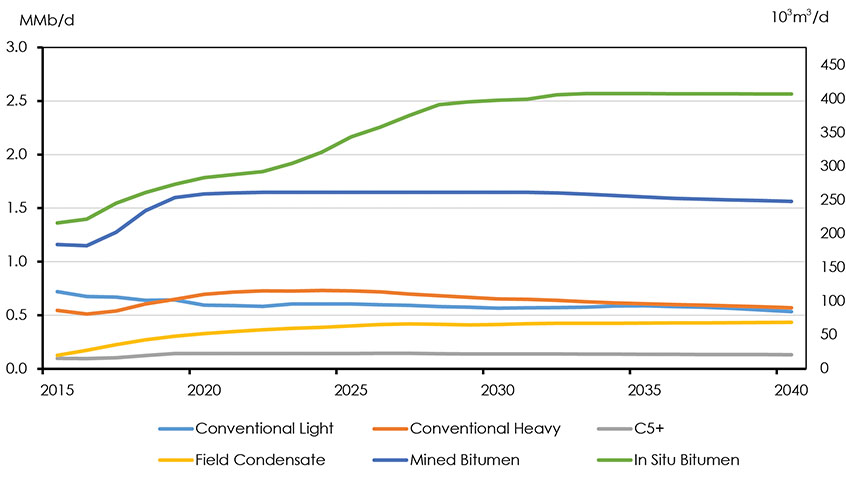

Another key factor is the relative lifetimes of oil sands projects versus other production types. Figure 4.24 shows production broken down by oil sands mining, in situ, and other production. Because of their long lifetimes, extremely low decline rates, and low per-barrel marginal costs of production, oil sands facilities continue to produce near current levels, with solvent-fueled technology leading to increases in production. Other forms of production, such as conventional and tight light oil, have shorter capital investment cycles, and are projected to be more responsive to global shifts in demand.

Figure 4.24: Oil Production by Type, Technology Case

Description

This chart shows oil production by type in the Technology Case from 2015 to 2040. Conventional light production decreases from 0.72 MMb/d in 2015 to 0.54 in 2040. Conventional Heavy rises from 0.55 MMb/d in 2015 to 0.73 in 2024 before falling to 0.57. C5+ production remains relatively stable and changes from 0.10 in 2015 to 0.13 in 2040. Field Condensate increases from 0.13 MMb/d to 0.44. Mined bitumen production increases from 1.16 MMb/d in 2015 until it peaks in 2022 at 1.65 before falling to 1.56. In situ bitumen production increases from 1.36 MMb/d in 2015 to 2.56 in 2040.

Electricity Generation

In the Technology Case, electricity generation is moderately higher than the Reference Case, reflecting improvements to energy efficiency roughly balancing additional electric demands from uses such as electric vehicles. In this case, Canada’s already low-emitting grid reduces its emission intensity even further.

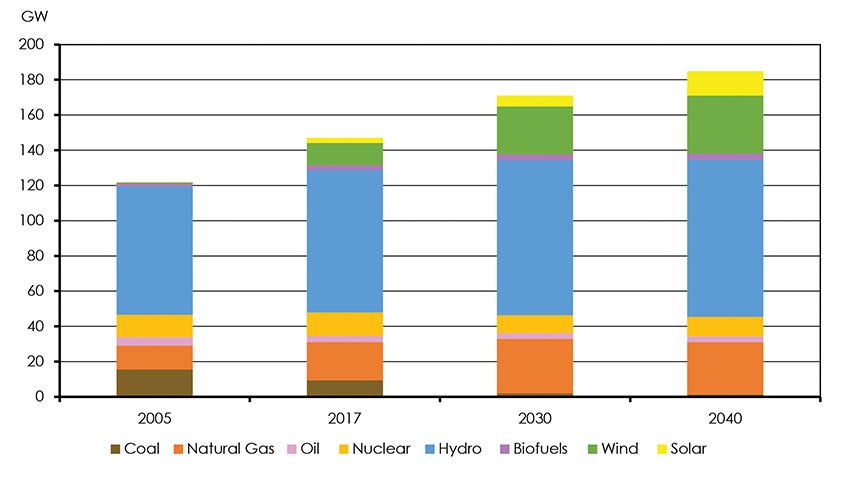

In the Technology Case, electric generating capacity is 26% higher than 2017 levels. Hydro still dominates Canada’s capacity mix, and the combined capacity of wind and solar more than triples in the Technology Case, due to assumed lower costs and improved integration. In the Technology Case, wind and solar make up over 25% of Canada’s capacity mix in 2040, compared to just over 10% in 2017. Figure 4.25 shows total electric capacity by fuel in 2005 and 2017 and in the Technology Case for 2030 and 2040.

Figure 4.25: Capacity 2005, 2017, Technology Case 2030 and 2040

Description

This graph shows Canadian generation capacity by type in the Technology Case in 2005, 2017, 2030, and 2040. In 2005 coal generation capacity was 15.5 GW, which fell to 9.3 in 2017, and is projected to continue falling to 2.0 in 2030 and 1.4 in 2040. Natural gas capacity increased from 13.6 GW in 2005 to 21.8 in 2017. In 2030 it increases to 30.9, then falls to 29.6 in 2040. Oil capacity continually falls from 4.7 GW in 2005 to 3.3 in 2040. Nuclear increased from 12.8 GW in 2005 to 13.3 in 2017, but is projected to fall to 10.2 in 2030 then increase 11.1 in 2040. Hydro capacity increases throughout the period from 72.9 GW in 2005 to 89.3 in 2040. Biofuels increase from 1.7 GW in 2005 to 3.4 in 2040. Wind capacity grows from 0.7 GW in 2005 to 13.7 in 2017, 27.2 in 2030, then to 34.0 in 2040. Solar also sees big gains and grows from 0 GW installed capacity in 2005, to 2.8 in 2017, 6.3 in 2030, and 13.7 in 2040.

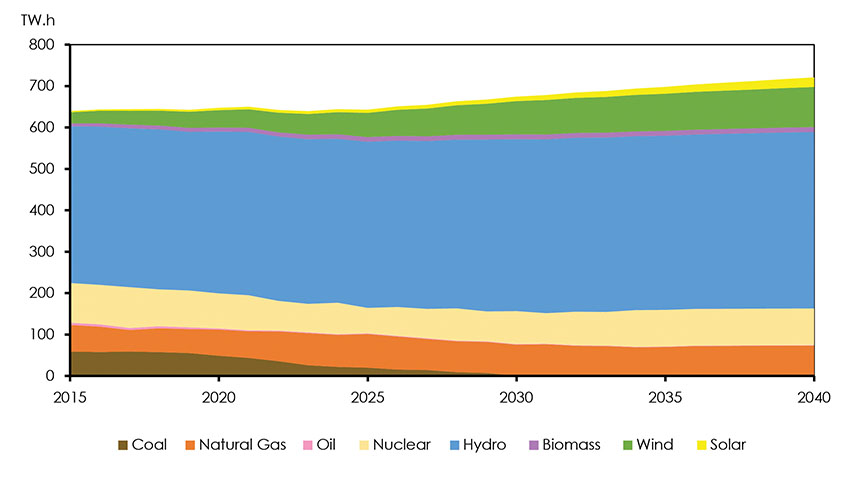

Electric generation is 12% higher than 2017 levels by 2040. Relative to the Reference Case, capacity grows more than generation in the Technology Case because most of the additions are wind and solar. Wind and solar tend to generate less per MW of capacity compared to other sources of electricity. While wind and solar make up 25% of capacity in 2040, these resources account for 17% of generation. Figure 4.26 shows electricity generation by source in the Technology Case.

Electricity generation varies significantly by province. For hydro generating provinces, the electricity mix is relatively similar to the Reference Case, with small levels of wind and solar added due to lower costs. For other provinces, wind and solar become an increasingly large part of the mix. These resources are backed up with natural gas as well as increased interchange and demand side management.

Figure 4.26: Electricity Generation by Fuel Type, Technology Case 2040

Description

This chart shows the change in generation by fuel in the Technology case from 2015 to 2040. Natural gas decreases from 40 TW.h to 73. Oil goes from 8 TW.h in 2015 to 1 in 2040. Coal falls from 94 TW.h 0. Nuclear rises from 87 TW.h to 8. Biomass also increases from 7 TW.h to 12. Solar rises from 0 TW.h to 23. Wind increases from 1.5 TW.h to 97. And hydro changes from 358 TW.h to 426.

Canada wide, the share of renewables and nuclear electricity generation reaches 90% by 2040. This compares to 84% in the Reference Case, and 82% in 2017. These annual figures can be misleading, as electric loads vary significantly during the day, as does available energy from variable sources like wind and solar. How these sources are matched with changes in electricity demands from end-users is an important uncertainty.

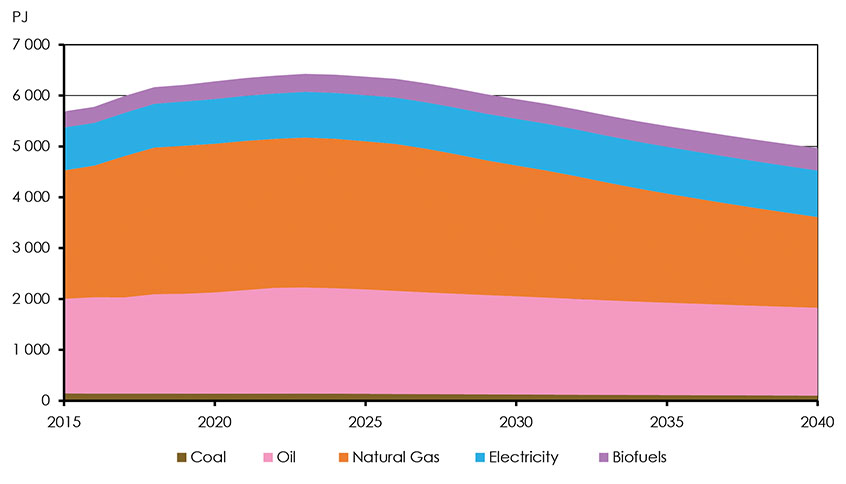

Primary Demand and GHG Emissions

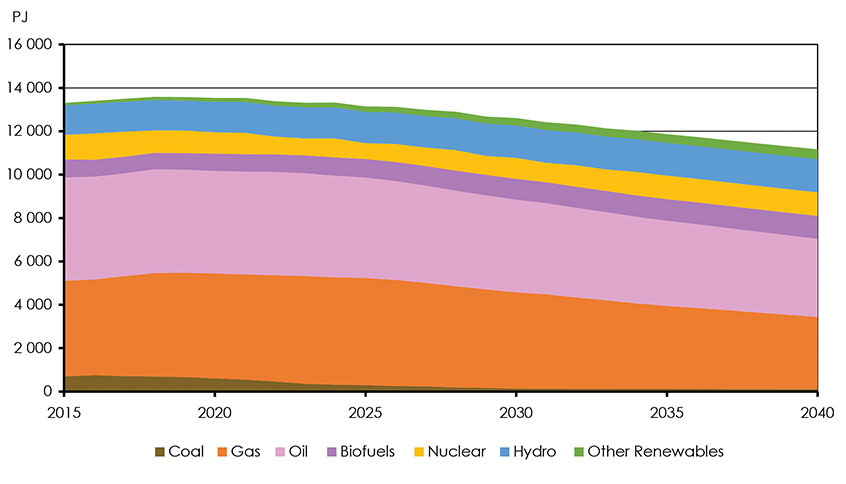

The Technology Case implies a significant reduction in total primary energy demand, as well as a shift towards relatively more non-emitting energy. These changes will reduce Canada’s GHG emission trajectory, as less fossil fuels are combusted and more carbon is captured and sequestered. Figure 4.27 shows total primary energy demand by fuel. In the near term, energy use peaks and then begins to decline, with energy demand in 2025 2 to 3% lower than 2017 levels. Post 2025, end-use electrification reduces direct fossil fuel use, improved efficiency reduces demands for all types of energy, and the electricity mix includes a greater share of renewable energy. Total primary energy use declines by over 1% per year from 2025 to 2040. By 2040, total demand is over 15% lower than 2017 levels, while fossil fuel use drops even faster to 30% below 2017 levels.

Figure 4.27: Primary Demand by Fuel

Description

This graph shows primary demand by fuel in the Technology case from 2015 to 2040. Coal demand drops from 690 PJ in 2015 to 108 in 2040. Natural gas demand decreases from 4415 PJ to 3340 in 2040. Oil demand changes from 4768 PJ in 2015 to 3606 in 2040. Biofuels demand increases from 833 PJ in 2015 to 1057. Nuclear demand falls from 1127 PJ to 1087. Hydro demand rises from 1363 PJ to 1533 by 2040. Demand for other renewables increases from 106 PJ in 2015 to 442 in 2040.

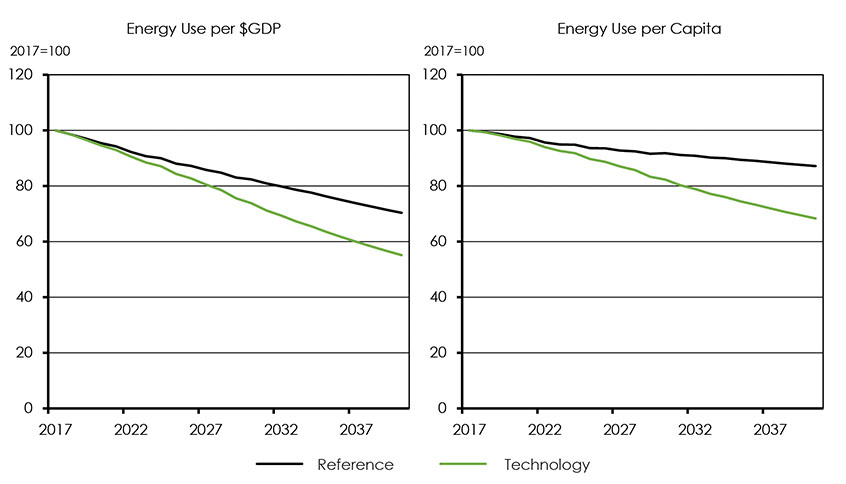

Figure 4.28 compares the total energy intensity of the economy between the Reference and Technology Cases, for both energy use per $ GDP and energy use per person. Energy use per $ GDP has generally declined in the last few decades, as economic growth has outpaced energy demand growth. Energy use per capita, on the other hand, has remained relatively flat. The Technology Case represents a further decoupling of energy use from GDP and population growth. This results in energy use per $ GDP declining 2.5% per year in the Technology Case, to be 45% lower than 2017 in 2040. Energy use per capita falls 1.6% per year in the Technology Case to be 30% lower than 2017 in 2040.

Figure 4.28: Energy Intensity Trends, Reference and Technology Cases, % of 2017 Level

Description

The chart on the left compares the energy use per $GDP in the Reference and Technology Cases relative to 2017. In the Reference Case intensity drops 30% and the Technology Case drops 45% by 2040.

The graph on the right shows the energy use per capita relative to 2017 for the Reference and Technology Cases. The Reference Case sees use drop by 13% and the Technology Case sees 31% drop.

Compared to the Reference Case, the Technology Case uses more renewable energy and less fossil fuels (Figure 4.29). Renewable additions include wind and solar for electricity generation, increased biofuel blending in transportation, and increased use of RNG in the natural gas mix. Fossil fuel reductions are due to fuel switching towards biofuels or electricity at the end use level, relatively less natural gas used to generate electricity, and efficiency and process changes that require less energy, such as the adoption of solvent technology in the oil sands or heat pumps in buildings.

Figure 4.29: Change in Primary Energy Demand by Fuel Type, Reference vs Technology

Description

This figure compares the change in primary energy demand by fuel type between the Reference and Technology Cases from 2015 to 2040. In 2040 coal use in the Technology Case is 58 PJ lower than in the Reference Case. Oil use is also 1068 PJ lower in the Technology Case by 2040, and natural gas use is 2368 PJ lower. Renewables on the other hand are 467 PJ higher in the Technology Case by 2040.

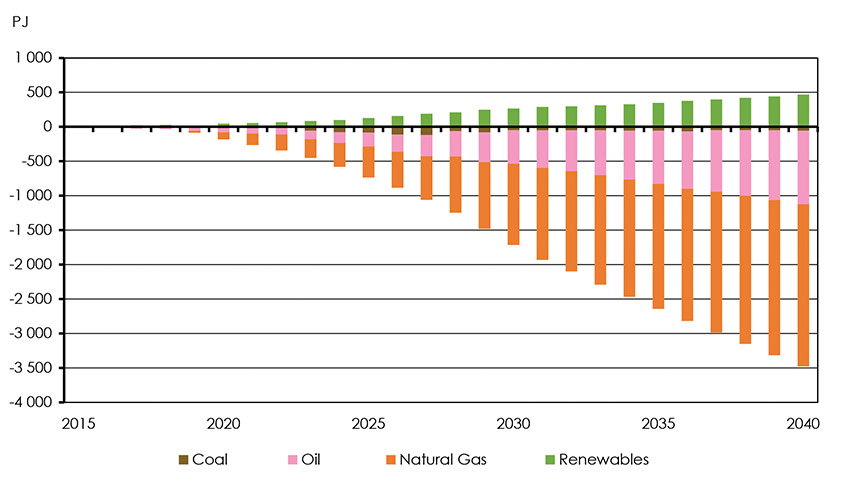

The Technology Case shows that in a transitioning global energy context, Canada’s energy mix will transition as well. Figure 4.30 illustrates the change in coal, oil product, and natural gas demand in five year increments over the projection. The near term shows trends for increasing fossil fuel use in Canada reversing, largely driven by coal retirements and improved vehicle efficiency reducing oil product demand. Natural gas increases in the near term due to its role in oil production, heating, and replacing some of the initial coal retirements. In the longer term, new technologies and strengthening policies reduce demand for all three, such that every five years fossil fuel demand drops by about 10%.

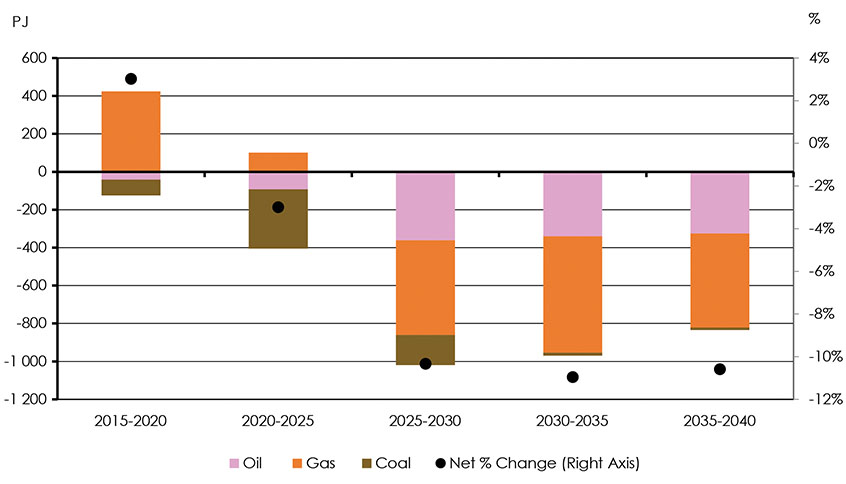

Figure 4.30: Change in Fossil Fuel Demand Over Five Year Increments, Technology Case

Description

This chart shows the change in fossil fuel demand broken down into 5 year increments in the Technology Case. From 2015-2020 oil and coal demand fall by 43 PJ and 83 respectively, while gas rises by 419 resulting in a net increase of 3%. In 2020-2025 oil and coal demand fall by 93 and 312 PJ, while gas demand increases by 104 PJ. The result is a net decrease of 3%. From 2025 to 2030 oil, natural gas, and coal fall by 361 PJ, 495, and 159. This results in a net decrease of 11%. From 2030 to 2035 oil, natural gas, and coal fall by 340 PJ, 610, and 15. This results in a net decrease of 11%. From 2035 to 2040 oil, coal, and natural gas fall by 325 PJ, 494, and 13. This results in a net decrease of 11%.

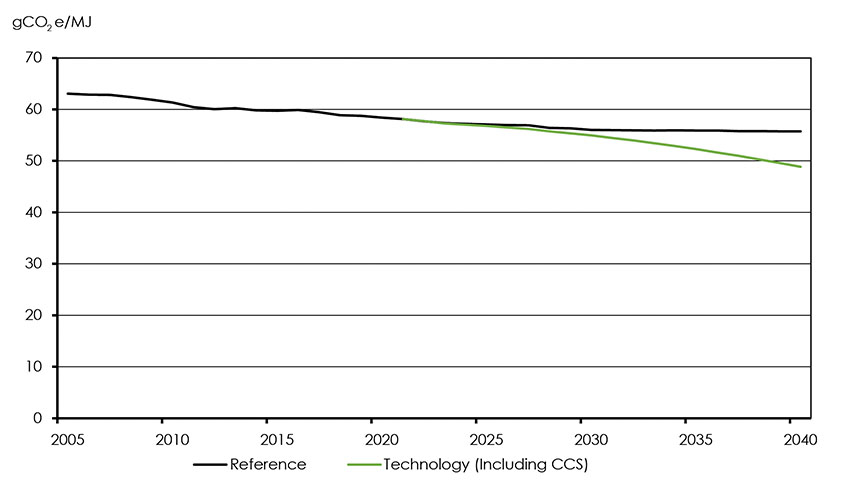

The combination of reduced coal, as well as increased CCS, reduces the GHG intensity of the fossil fuel mix, putting further downward pressure on Canadian GHG emissions. Figure 4.31 compares estimated fossil fuel GHG emissions intensity for the Reference and Technology case.

Figure 4.31: Estimated Fossil Fuel GHG Emissions Intensity, Reference and Technology Cases

Description

This chart shows the projected changes in fossil fuel GHG emission intensity in the Reference and Technology Cases from 2005 to 2040. Both the Reference Case and Technology Case begin with an intensity of 63 gCO2e/MJ. The Reference Case then declines to 56 gCO2e/MJ, while the Technology Case falls to 49 gCO2e/MJ by 2040.

Key Uncertainties

The Technology Case provides one snapshot of what a global shift towards a low carbon economy might mean for Canada. Future development of both policies and technologies could lead to different outcomes than those presented in this analysis.

- Global context: How the global context affects global energy markets and investment is a key uncertainty that is important for the oil and gas projections. In the case of oil, others have suggested that falling global oil demand would mean a lower price than the Technology Case assumes. This could bring Canadian production trends closer to the Low Price Case.

- Differentials and infrastructure: Regional price differentials and infrastructure developments are generally assumed to be similar to Reference Case levels in the Technology Case. These are all highly uncertain areas however. Both oil and gas differentials could be different than assumed here, as could impact future project developments like LNG.

- Lower technology costs: The Technology Case assumes that costs of new technologies such as wind, solar, and batteries will continue to fall in the longer term. If these reductions do not occur, it is likely the adoption of these technologies will be lower.

- Increased end-use electricity: As part of the Technology Case, many end-use applications switch to electricity. Although the overall results of the Technology Case show similar electricity demand with the Reference Case as improved efficiency balances additional demand sources, there are many uncertainties with this result. First, depending on the distribution of electric loads throughout the day, or season, there may be additional challenges for the electric grid. Second, other scenarios see electricity increasingFootnote 26 as additional load requirements may not be offset by improved efficiency.

- Technological innovation: There are many details that are not covered in this analysis, which is based on relatively high level trends. As new technologies are adopted, the integration of energy supply and demand will likely become more and more important. Innovation will be necessary across the entire spectrum of the energy system–consuming and producing technologies, market and policy design, and public involvement in energy system issues– to ensure Canadians’ energy needs are met in a reliable and affordable way.

- Disruptive technologies: The EF2018 Technology Case generally assumes gradual adoption of new technologies. Faster changes and disruptive technologies could alter the way Canadians use and produce energy, resulting in primary energy demand that is lower or higher in any of the cases presented in this report.

- Date modified: