Market Snapshot: Critical Minerals are Key to the Global Energy Transition

Connect/Contact Us

Please send comments, questions, or suggestions for Market Snapshot topics to snapshots@cer-rec.gc.ca

Release date: 2023-01-18

What are critical minerals?

Critical minerals are minerals that are essential to modern-day technologies, including renewable electricity, batteries, electronics, and electric vehicles.Footnote 1 What is defined as a critical mineral is usually determined by the mineral’s strategic importance to a country, as well as the availability of supply, the demand, and the existence of viable substitutes. The list of critical minerals varies by country. Canada’s current list, as seen in the infographic below, contains 31 minerals.Footnote 2 The list is used to develop policy and prioritize mining-related investments.

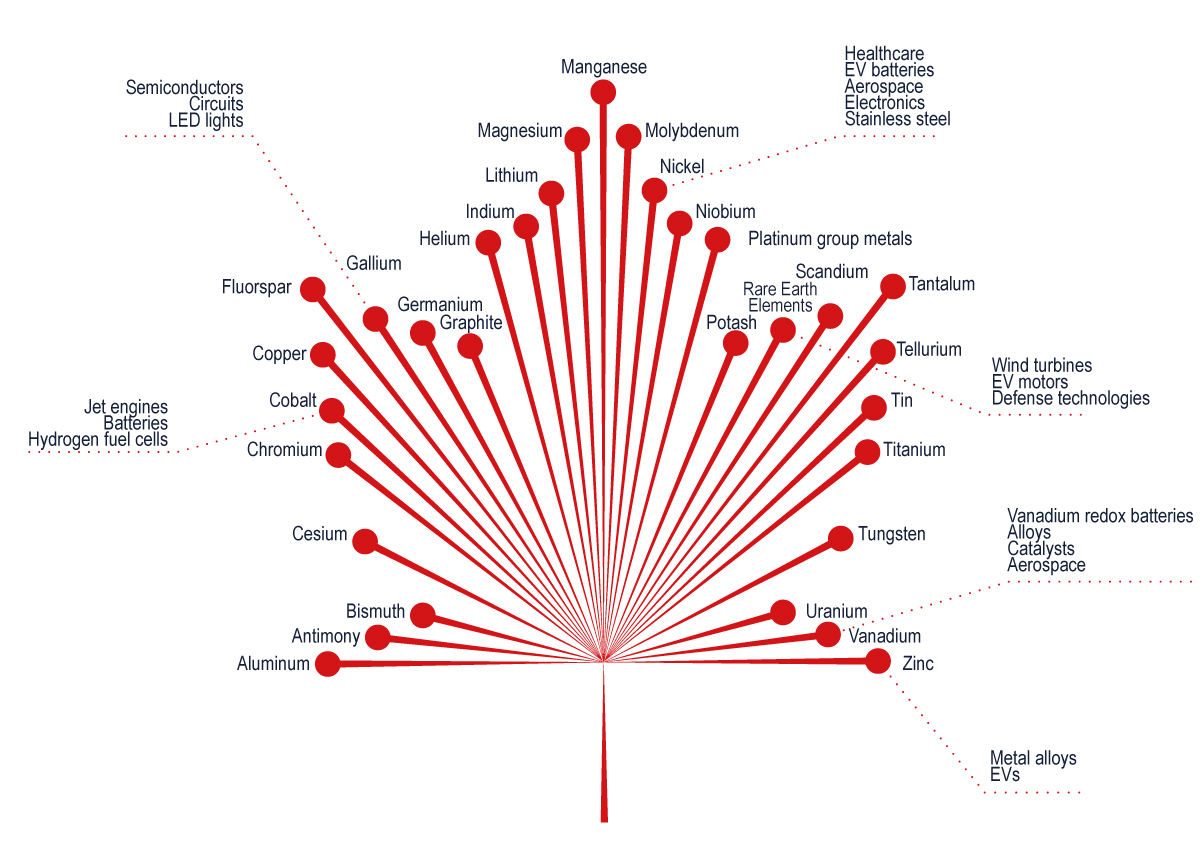

Figure 1: Canada’s list of 31 critical minerals and their usesFootnote 3

Source and Description

Source: Natural Resources Canada

Description: List of 31 critical minerals depicted in the shape of a maple leaf. The critical minerals are listed with some examples provided. The 31 critical minerals are:

- Aluminium

- Antimony

- Bismuth

- Cesium

- Chromite

- Cobalt (Examples are jet engines, batteries and hydrogen fuel cells)

- Copper

- Fluorspar

- Gallium (Examples are semiconductors, circuits and LED lights)

- Germanium

- Graphite

- Helium

- Indium

- Lithium

- Magnesium

- Manganese

- Molybdenum

- Nickel (Examples are healthcare, EV batteries, aerospace, electronics and stainless steel)

- Niobium

- Platinum group metals

- Potash

- Rare earth elements (Examples are wind turbines and defense technologies)

- Scandium

- Tantalum

- Tellurium

- Tin

- Titanium

- Tungsten

- Uranium

- Vanadium (Examples are vanadium redox, batteries, alloys, catalysts and aerospace)

- Zinc (Examples are metal alloys and EVs)

Future demand for critical minerals

Global demand for critical minerals and the products they are manufactured into is likely to increase significantly in coming decades. The International Energy Agency estimates that, in response to global efforts to reach the climate goals of the Paris Agreement,Footnote 4 mineral demand for clean technologies will increase by two to six times by 2040, when compared to 2020.Footnote 5

Figure 2 shows how demand may evolve depending on the International Energy Agency’s different scenarios. Most growth in demand will be from expanding fleets of electric vehicles and battery storage, as well as expanding electricity networks.Footnote 6 Low-emission electricity generation, such as renewables, tend to rely more on critical minerals than other types of power generation.Footnote 7

Figure 2: Global minerals demand for clean energy technologies, 2020 compared with 2040 scenariosFootnote 8

Source and Description

Source: International Energy Agency – The Role of Critical Minerals in Clean Energy Transitions

Description: This stacked bar chart shows the estimated demand of critical minerals by clean technology (solar, wind, electric vehicles and battery storage, electricity networks, hydrogen, and other low-carbon power generation) in 2020 and in 2040 under three IEA policy scenarios (Stated Policies, Sustainable development, and Net-zero by 2050).

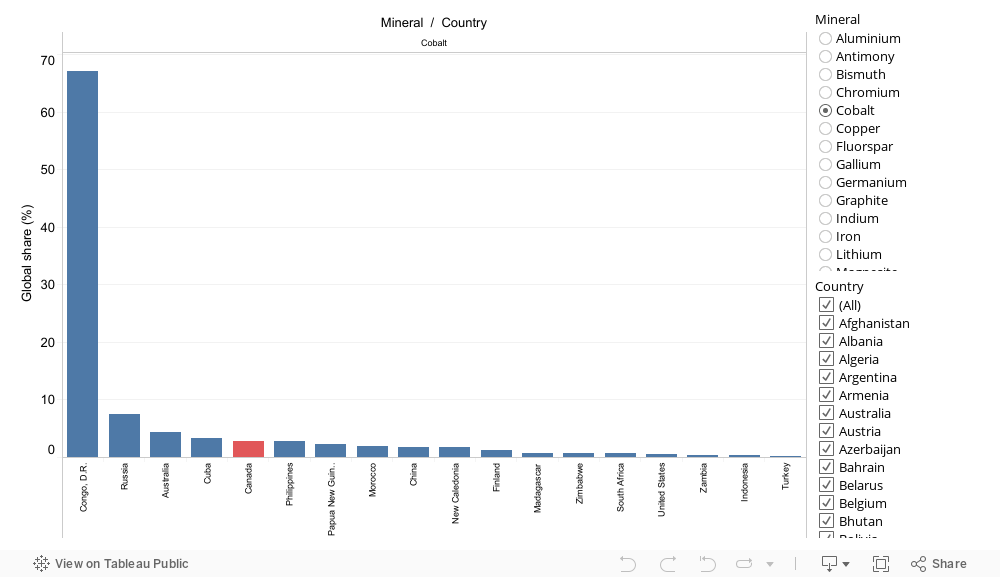

Global mineral production

While all countries require some critical minerals, production (mainly mining and processing) is concentrated more in some countries than in others. For example, in 2020, China produced 57% of global aluminum, while the Democratic Republic of Congo produced 67% of cobalt. Chile produced 28% of copper, Australia 48% of lithium, and Canada 31% of potash.

Figure 3 shows the share (in percentage) of global production of selected critical minerals by country for 2020.

Figure 3: Share of mineral production by mineral and country (2020)

Sources and Description

Sources: World Mining Data and World Nuclear Association

Description: This chart shows the share (in percentage) of global production of selected minerals by country, for 2020. The blue columns represent individual countries’ share of global production. Canada’s share is represented by a red column.

Concentration of mineral production in a few countries makes supply more vulnerable to environmental, economic, and geopolitical risks.Footnote 9 This vulnerability, along with rising demand and limited production capacity for these critical minerals, has caused recent and significant price increases. For example, the price of lithium increased by 738% between January 2021 and March 2022, while cobalt increased by 156% and aluminum by 76%.Footnote 10

Canada seeks to assert itself as the leading mining nation. The recently released Canada’s Critical Minerals StrategyFootnote 11 illustrates how Canada intends to responsibly increase critical minerals production and support the development of domestic and global value chains.

Canada already produces over 60 minerals and metals and is a top five global producer of 14 mineral and metal products:Footnote 12

- potash (world’s largest producer)

- niobiumFootnote 13 (second largest producer)

- diamondsFootnote 14Footnote 15 (third largest producer)

- indiumFootnote 16 (fourth largest producer)

- uraniumFootnote 17 (third largest producer)

- palladium (third largest producer)

- primary aluminum (fourth largest producer)

- platinum (fourth largest producer)

- cadmiumFootnote 18 (fourth largest producer)

- wollastoniteFootnote 19 (fourth largest producer)

- titanium concentrate (ilmenite) (fourth largest producer)

- gold (fifth largest producer)

- telluriumFootnote 20 (fifth largest producer)

- cobalt (fifth largest producer)

- Date modified: