Canada’s Pipeline Transportation System 2016

Maritimes & Northeast Pipeline LP.’s Maritimes & Northeast Pipeline

| Commodity and NEB Group | Natural Gas (Group 1) |

| Annual average capacity | 16 106m³/d (0.56 Bcf/d) |

| Average utilization 2015 | 45% |

| Primary receipt points | Goldboro, NS |

| Primary delivery points | Halifax, NS; Moncton, Saint John, St. Stephen, NB |

| Rate base 2015 | $401 million |

| Cost of Service 2015 | $120 million |

| Abandonment Cost Estimate and Collection PeriodNote a | $150 million; 19.5 years |

Source: NEB

Text version of this map

This map provides an overview of the Maritimes & Northeast Pipeline.

Overview

The Maritimes & Northeast Pipeline (M&NP) in Canada extends from Goldboro, NS through New Brunswick to a point on the Canada-U.S. border near St. Stephen, NB. In the U.S., M&NP continues through Maine and New Hampshire into Massachusetts. It interconnects with the Emera Brunswick Pipeline, Portland Natural Gas Transmission System, Tennessee Gas Transmission, and Algonquin Gas Transmission.

M&NP was commissioned in December 1999 to transport natural gas produced from the Sable Offshore Energy Project (Sable) to markets in the U.S. Northeast. It currently also transports offshore natural gas from the Deep Panuke project, and supply from the McCully gas field in New Brunswick. M&NP can flow bi-directionally and natural gas will flow from the U.S. into Canada when offshore production is insufficient to meet domestic demand. Incremental supply comes from the Canaport LNG import terminal via the Brunswick Pipeline or from the Portland Natural Gas Transmission System.

Key Developments

Natural gas supply from offshore Nova Scotia declined in 2015. In mid-May, production at Deep Panuke was shut-in and Encana (the operator) announced that the project would produce only during the winter months when demand and gas prices are highest. In addition, Deep Panuke’s reserve estimate was cut by half due to higher than expected water incursion into the reservoir. Production at Sable in 2015 remained steady averaging 4 106m³/d (0.14 Bcf/d); however, the project is in long-term decline.

Utilization

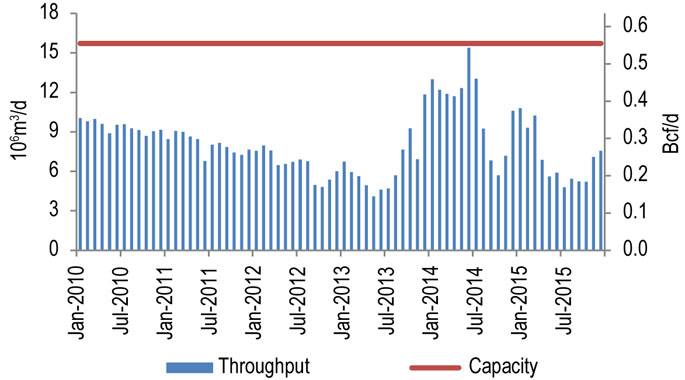

Figure 10.7.1 shows capacity and throughput on M&NP for 2010-2015. Capacity is 16 106m³/d (0.56 Bcf/d) and in 2015, throughput (exports and imports) averaged 7 106m³/d (0.25 Bcf/d).

Figure 10.7.1: M&NP Throughput vs. Capacity

Sources: Maritimes & Northeast Pipeline, NEB

Text version of this graphic

This bar chart shows throughput and capacity on the Maritimes & Northeast Pipeline between 2010 and 2015. Capacity in 2015 was 16 106m³/d (0.56 Bcf/d). Throughput averaged 7 106m³/d (0.25 Bcf/d) in 2015, compared to 11 106m³/d (0.39 Bcf/d) in 2014.

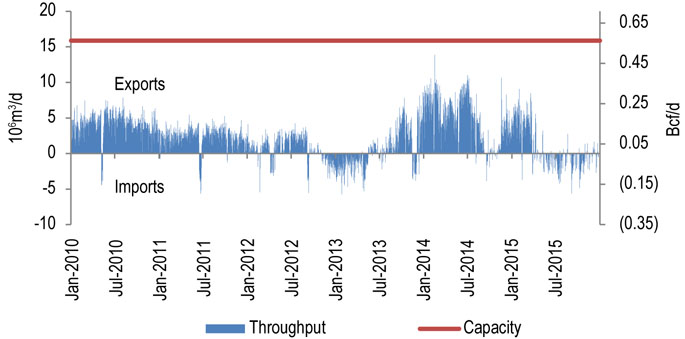

Figure 10.7.2 shows capacity and daily throughput on M&NP at the St. Stephen, NB point. Traditionally, the Maritimes market was a net-exporter of natural gas to the U.S. However, during periods of high demand or when offshore production is insufficient to meet domestic demand, the flow of natural gas on M&NP is reversed and natural gas is imported into the Maritimes from the U.S. Since the spring of 2015, the Maritimes has primarily been a net-importer of natural gas from the U.S.

Figure 10.7.2: M&NP Daily Throughput at St. Stephen

Sources: Maritimes & Northeast Pipeline, NEB

Text version of this graphic

This bar chart shows throughput and capacity at the St. Stephen import/export point on the Maritimes & Northeast Pipeline between 2010 and 2015. Capacity in 2015 was 16 106m³/d (0.56 Bcf/d). Throughput varied in 2015, with exports to the U.S. occurring mostly at the beginning and end of 2015. Imports occurred primarily during the spring and summer months.

Tolls

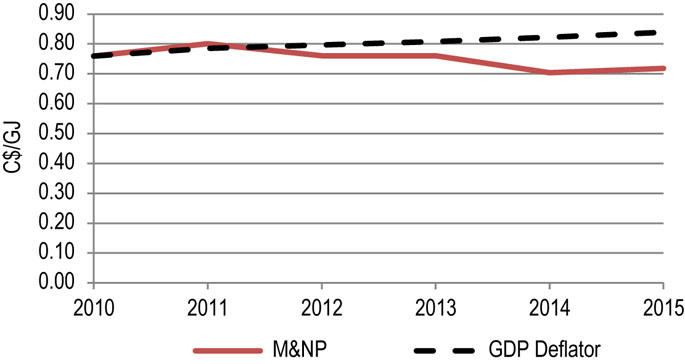

M&NP uses a ‘postage stamp’ tolling model in which the toll is the same for all paths on the system regardless of the distance travelled. M&NP has been operating under a toll settlement for 2014-2016. Figure 10.7.3 shows M&NP’s benchmark toll (MN365 Toll) and the GDP deflator (normalized) for 2010-2015. The benchmark toll declined slightly in 2012 and 2013 due to lower revenue requirements, and in 2014 as the rate base decreased with depreciation.

Figure 10.7.3: M&NP Benchmark Toll

Source: NEB toll filings

Text version of this graphic

This graph shows the M&NP benchmark toll as a solid red line and the GDP deflator as a black dashed line. The benchmark toll decreased slightly over the period from $0.76 in 2010 to $0.72 in 2015.

Financial

Maritimes & Northeast Pipeline L.P.’s financial ratios have improved due to the reduction of debt over time. DBRS has maintained its credit rating at “A” due to its predictable cash flows which are a result of firm transportation contracts with investment grade shippers, a backstop provided by ExxonMobil Canada, and a tolling methodology that is regulated on a cost of service basis.

| Maritimes & Northeast Pipeline L.P. | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|---|---|

| Revenues (millions) | $140.7 | $142.4 | $133.3 | $138.7 | $141.6 | $119.9 |

| Fixed Costs (millions) | $23.9 | $25.1 | $24.7 | $23.0 | $26.0 | $25.9 |

| Rate Base (millions) | $591.3 | $571.3 | $528.0 | $492.3 | $445.2 | $401.4 |

| Return on Equity | 6.45% | 5.96% | 5.55% | 5.51% | 6.87% | 7.32% |

| Interest and Fixed-Charges Coverage RatioNote a | 3.41 | 2.78 | 2.8 | 3.03 | 3.49 | 3.79 |

| Cash Flow to Total Debt and Equivalents RatioNote a | 22.2% | 23.9% | 25.9% | 30.2% | 38.8% | 42.6% |

| DBRS Credit Rating | A | A | A | A | A | A |

| Moody’s Credit Rating | A2 | A2 | A2 | A2 | A2 | A2 |

- Date modified: